Retirement Living takes an unbiased approach to our reviews. We may earn money when you click a partner link. Learn More

Coventry Direct Review

4.5 Overall Rating

Ease of Use

Customer Service

Qualifications

Costs

Bottom Line

Simplified Settlements, which is part of Coventry Direct, streamlines the underwriting process. Life settlements typically close within 30 days of when you submit all information. Those who own policies worth $100,000 to $500,000 can use Simplified Settlements. You can submit information about your life insurance on Coventry’s website to begin the process of selling your policy.

Updated:

About Coventry Direct

Simplified Settlements, which is part of Coventry Direct, streamlines the underwriting process. Life settlements typically close within 30 days of when you submit all information. Those who own policies worth $100,000 to $500,000 can use Simplified Settlements. You can submit information about your life insurance on Coventry’s website to begin the process of selling your policy.

Coventry conducted the first life settlement transaction, and in the 40 years since then, has taken the lead in supporting the highest standards of conduct across the industry. The company and its affiliates bought more than three times as many life insurance policies as its closest competitor in 2021. The company fosters a collaborative environment, and its team members prioritize customer education.

Pros

- Long-standing industry reputation

- Option for retained death benefit

- 30-day close

Cons

- Minimal details on the company’s website

How to Sell Your Policy With Coventry

After talking with a policy specialist on the website’s chat feature, we learned that it’s easy to figure out if you can sell your life settlement policy to Coventry.

Simply fill out a form with basic information, such as the amount, type, age of the policy (a range is fine), and the insurance company’s name. It can take about two weeks to get an offer after you submit your request, and if you accept the offer, you’ll get your money in 30 to 45 days.

In general, you’ll follow this process to sell your policy with Coventry:

- Complete the questionnaire on the website.

- Coventry will value the policy to determine if they can make an offer.

- Coventry will relay the offer to the advisor.

- Once you accept the offer, Coventry will issue closing documents.

- After receiving the executed closing documents, Coventry will send the change of ownership and beneficiary forms to the life insurance company.

- The carrier will confirm they’ve processed the change forms and will release the funds to you.

Coventry offers retained death benefits options and simplified settlements to customers facing financial hardship. With retained death benefits, you can keep a portion of your life insurance with no future premiums. Coventry’s simplified settlement process can help you turn smaller, unneeded policies between $100,000 and $500,000 into cash.

| Retained Death Benefit Option | – Choose to keep a portion of the death benefit instead of a cash payment. – Receive a cash settlement and retain a portion of the death benefit. – Redesign death benefit if the need for insurance decreases over time. |

| Simplified Settlements | – Streamlined underwriting process in less than 30 days. – Helpful for realizing the value of smaller policies. |

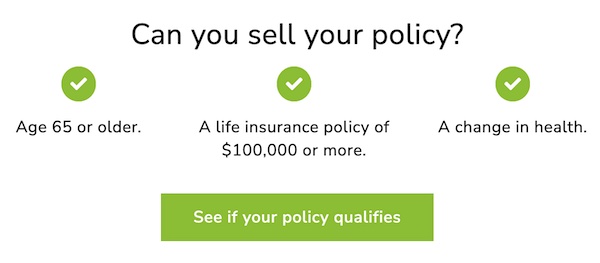

Who Qualifies for a Life Settlement?

To sell a life insurance policy, you’ll need to meet minimum qualifying factors. Most companies who buy policies look for those 65 or older with a death benefit of $100,000 or more. Those with a life expectancy of up to 20 years have better approval odds.

Significant health impairments or a decline in health from the time your policy was issued might improve your chances, but the ability to sell your policy will depend on the provider or broker.

Coventry Direct FAQs

A life settlement is the sale of a life insurance policy by the policy owner to a third party. The seller typically gets more than the policy’s cash value but less than the death benefit amount. The third party will pay the policy’s premiums and collect the death benefit when the insured dies. Most states require you to hold your life insurance policy for two to five years before selling it.

If you have a term or universal life insurance policy, you can use a life settlement company—but age, policy, and health qualifiers apply. Coventry will purchase life insurance policies valued at $100,000 or more from individuals aged 65 or older.

Financial publication The Deal consistently ranks Coventry No. 1 for life settlements by number and value. A leader in the market for life insurance, Coventry hires knowledgeable financial representatives and customer specialists to help speed up and simplify the transaction process. The company has delivered more than $5 billion to policyholders who no longer need their life insurance.

Coventry purchases active life insurance policies from seniors. Upon purchase, Coventry becomes the beneficiary and pays the premiums. Then, Coventry will sell the policies to investors or maintain them to collect the death benefits later.

Coventry Direct builds education into their processes, evaluating policies for free and with no commitment, as many people do not understand that you can sell your unneeded insurance policies rather than surrendering them or letting them lapse.

You can sell universal life, whole life, variable life, survivorship, group life and even term life policies with Coventry.

Conclusion

Coventry is the industry’s biggest life settlement provider. Its size, sound reputation, and numerous industry accolades make it a top choice for consumers who want to sell their policies quickly and effectively.