How Much Does a $300,000 Annuity Pay Per Month?

Updated:

Open Access

In 2023, U.S. annuity sales reached $350 billion, highlighting their growing role in retirement planning. A $300,000 annuity can provide $1,800 monthly at age 60, $1,983 at 65, or $2,138 at 70.

This guide breaks down annuity payouts, helping you understand what to expect based on your age and financial goals.

Key Insights

A $300,000 annuity can provide $1,800 monthly at age 60, $1,983 at 65, or $2,138 at 70.

↓ Jump to insight

Indexed annuities experienced a 22.5% increase, contributing an additional $10.9 billion compared to the first six months of 2023.

↓ Jump to insight

For a $200,000 annuity, At age 65, a male would receive $1,258 per month, while a female would receive $1,199 per month.

↓ Jump to insight

At age 75, the IRR reaches 3% by year 10 and exceeds 5% by year 20.

↓ Jump to insight

By late 2024, total U.S. retirement assets reached $42.4 trillion, with IRAs accounting for $15.2 trillion, a 4.6% increase from the previous quarter.

↓ Jump to insight

What Is a $300,000 Annuity?

A $300,000 annuity is a financial product that provides guaranteed monthly income to the annuitant, making it a popular choice for retirees seeking stability. The amount you receive depends on factors like your age, gender, and the type of annuity.

For instance, a 65-year-old woman with an immediate annuity might receive $1,798 per month. However, if you opt for a deferred income annuity where monthly payments begin later, typically at 75 or 80, the monthly income can significantly increase.

For example, a 65-year-old man starting payments at age 80 could get $4,000 per month, while a woman of the same age might receive around $3,500 per month.

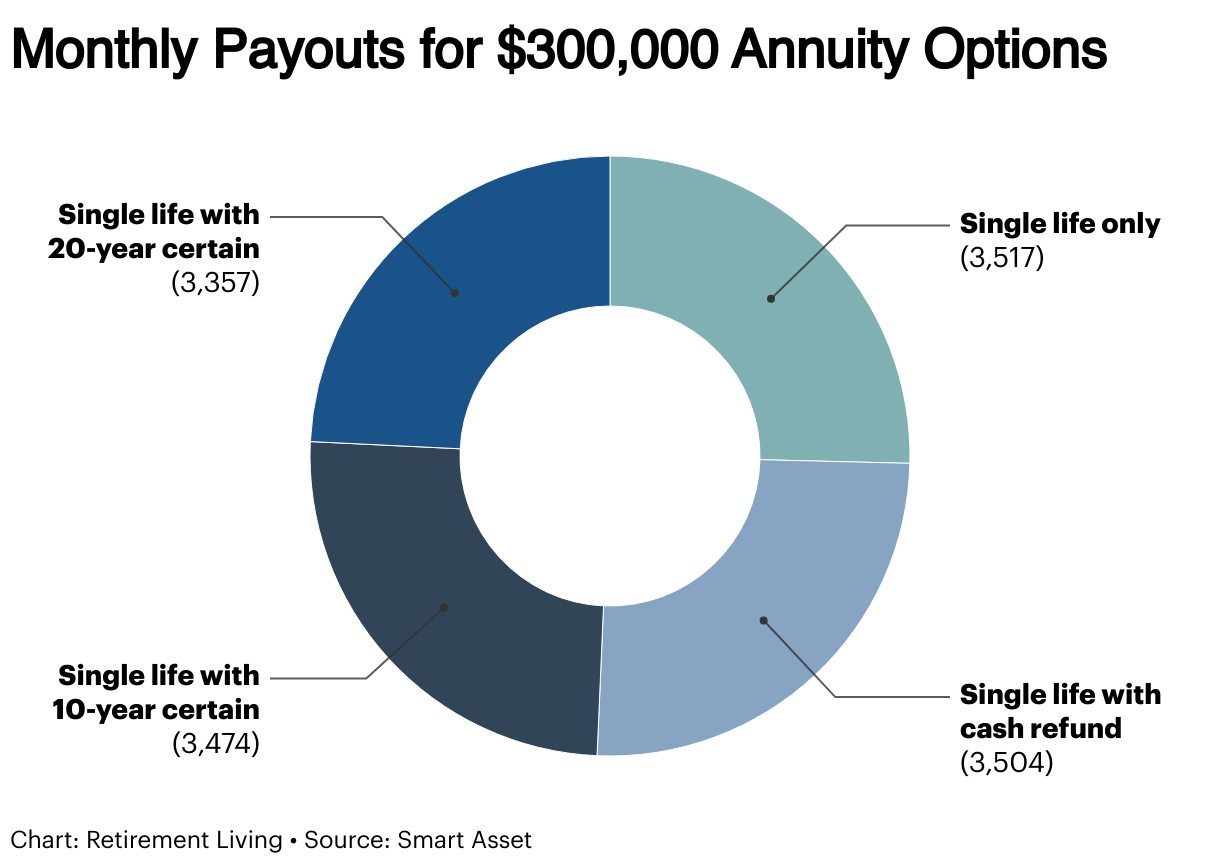

According to the Annuity Calculator, when choosing a $300,000 fixed annuity, the annuity company typically has four payout options, each offering different benefits and income amounts:

- $3,517 per month: Single life only (lifetime income, no death benefit).

- $3,474 per month: Single life with a 10-year certain (lifetime income with a 10-year payment guarantee for beneficiaries).

- $3,357 per month: Single life with a 20-year certain (extends beneficiary payments to 20 years).

- $3,504 per month: Single life with a cash refund (lifetime income and a lump-sum refund to beneficiaries).

Choosing the right option depends on your financial goals and priorities, whether that’s maximizing your lifetime income or leaving a legacy for your loved ones.

Recent Trends in Annuities

The annuities market has seen significant growth, driven by increasing demand for secure retirement income. In the first half of the year, fixed-rate deferred annuities rose by 16.3% year over year, adding $11.7 billion in premiums.

Meanwhile, indexed annuities experienced a 22.5% increase, contributing an additional $10.9 billion compared to the first six months of 2023.

Registered index-linked annuities grew by a staggering 41.7%, reflecting a premium increase of $9.1 billion during the same period. This trend highlights the growing popularity of products offering both market-linked returns and downside protection.

Monthly payouts have also risen. For example, a 65-year-old man purchasing a $100,000 single-life annuity with a 10-year guarantee saw payouts increase by 20.5% from $475 in January 2022 to $572.57 in February 2023.

This growth reflects improved rates and heightened competition among providers.

How Much Does a $75,000 Annuity Pay Per Month?

According to the Annuity Expert, a $75,000 annuity offers monthly payouts that vary based on age. As of January 2025:

- At age 60, you’ll receive $450 per month.

- At age 65, the payout increases to $496 per month.

- At age 70, monthly payments rise to $534.

For larger annuities, payouts follow a similar pattern of growth with age. For example, a 60-year-old male with a $750,000 annuity receives $4,286 per month, while at age 80, the payout jumps to $7,682 per month, which is a 79% increase.

Similarly, for females, payouts rise from $4,128 at age 60 to $7,042 at age 80, reflecting a 70% increase.

This steady rise in payouts demonstrates the value of delaying annuity payments, as older ages result in significantly higher monthly income.

How Much Does a $100,000 Annuity Pay Per Month?

A $100,000 annuity provides monthly payouts that depend on your age and payment structure. As of January 2025:

- At age 60, you’ll receive $600 per month.

- At age 65, this increases to $660 per month.

- At age 70, monthly payouts rise to $713.

For lifetime annuities, age plays a significant role in determining payouts:

- A 60-year-old male receives $572 per month, while an 80-year-old male gets $1,024 per month, a 79% increase.

- For females, payouts rise from $550 at age 60 to $939 at age 80, reflecting a 71% increase due to longer life expectancy.

Joint-life annuities, designed to provide income for both spouses, offer lower payout amounts:

- At age 60, joint life pays $505 per month, compared to $572 for males or $550 for females.

- At age 80, joint life pays $781, less than $1,024 for males or $939 for females.

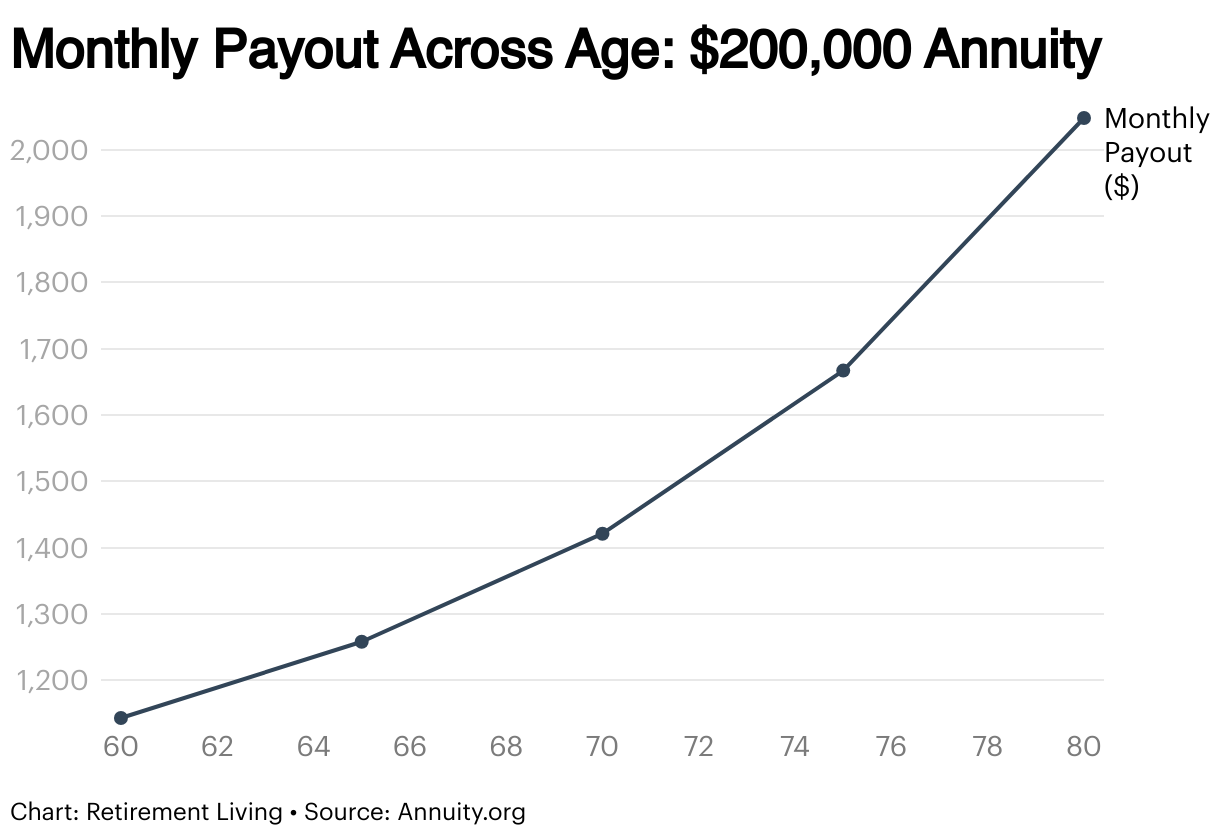

How Much Does a $200,000 Annuity Pay Per Month?

A $200,000 annuity provides varying monthly payouts depending on your age and payment structure. For example, as of January 2025:

- At age 60, you can expect $1,200 per month.

- At age 65, this increases to $1,322 per month.

- At age 70, monthly payouts rise to $1,425.

Gender and life expectancy also play a role. At age 65, a male would receive $1,258 per month, while a female would receive $1,199 per month, reflecting women’s longer average life expectancy.

For a 65-year-old couple, a joint-life annuity pays $1,083 per month, less than the single-life payouts, as benefits are designed to last until both individuals pass away.

For males, the monthly income payments rise steadily with age:

- $1,143 at 60

- $1,258 at 65

- $1,421 at 70

- $1,667 at 75

- $2,048 at 80

Factors Influencing Monthly Payouts

When determining how much an annuity pays each month, several factors come into play. These include the annuitant’s life expectancy, the payout period, the type of annuity, and prevailing interest rates. Here’s a breakdown:

Annuitant’s Life Expectancy

Your age and gender heavily influence monthly payouts. Insurance companies calculate your expected lifespan to decide payment amounts:

- If you’re expected to live longer, your monthly payments will be smaller to stretch the income over time.

- While the total payout isn’t guaranteed, you’re assured income for the rest of your life. Those who live more years than expected may receive more than the annuity’s original value.

Purchasing an annuity between ages 70 and 80 often yields the best Internal Rate of Return (IRR):

- At age 75, the IRR reaches 3% by year 10 and exceeds 5% by year 20.

- At age 70, IRRs also improve quickly, becoming positive faster than for younger buyers.

Payout Period

The length of time payments are guaranteed impacts the amount you receive each month:

- Single-life annuities pay higher amounts because they stop when the annuitant passes away.

- Joint-life annuities cover two lifetimes, so the monthly payouts are lower.

Payout annuities also gained popularity in recent years. In 2022, sales increased by 25% to $755 million, up from $604 million in 2021. Within this category, joint-life annuity sales grew by 6.5%, while single-life annuities saw an 18% increase.

Type of Annuity

The kind of annuity you choose affects how predictable your payouts will be:

- Immediate annuities offer straightforward and consistent payments.

- Deferred annuities involve an accumulation phase, making returns harder to predict upfront.

Immediate annuities are the best annuity option for those who want reliable income without delays or complexities.

Interest Rates

Interest rates directly impact annuity payouts. Since annuities are tied to bond market performance, changes in rates affect the returns insurers can offer. As of January 2025, the U.S. benchmark interest rate stands at 4.50% and is expected to remain steady. Higher interest rates typically lead to better annuity payouts because insurers can earn more from bonds backing their contracts.

Annuities vs. Other Retirement Income Options

When planning your retirement, annuities are just one option among several income sources. Here’s how they compare with other popular choices like Social Security, IRAs, pensions, and 401(k)s.

Social Security

While Social Security provides a predictable stream of income, it often isn’t enough to cover all expenses. That’s where annuities and other options can help fill the gap.

In 2025, Social Security benefits for retirees will see slight increases:

- The maximum monthly benefit at full retirement age rises to $4,018, up from $3,822 in 2024.

- The average monthly benefit for retired workers increases from $1,927 to $1,976, while couples’ benefits grow to $3,089.

IRAs

Individual Retirement Accounts (IRAs) and annuities both offer tax advantages, but their roles differ:

- IRAs are investment vehicles that hold assets such as from the stock markets, bonds, or mutual funds.

- Annuities are insurance products specifically designed to generate income.

By late 2024, total U.S. retirement assets reached $42.4 trillion, with IRAs accounting for $15.2 trillion, a 4.6% increase from the previous quarter. IRAs give you more flexibility in choosing investments, while annuities provide a fixed or predictable income stream.

Pensions

Pensions are becoming less common, but they remain a reliable source of income for some retirees. Around one-third of older adults receive pension income and the median yearly benefit is $11,040 for private pensions and $24,980 for state or local government pensions.

Unlike pensions, annuities are customizable and reliant upon the insurance company. You can choose how and when to start receiving payouts, but they may offer fewer investment options compared to pensions.

401(k) Plans

A 401(k) is a tax-deferred retirement savings account offered by many employers:

- Contributions are often deducted directly from your paycheck.

- Traditional 401(k)s are funded with pre-tax dollars, while Roth 401(k)s use after-tax contributions.

By the end of 2023, 70 million active participants were enrolled in 401(k) plans. The flexibility of 401(k)s allows you to decide how funds are invested and withdrawn during retirement. However, unlike annuities, 401(k)s don’t guarantee lifetime income.

Bottom Line

In 2023, U.S. annuity sales reached $350 billion, emphasizing their growing importance in retirement planning. A $300,000 annuity can provide $1,800 monthly at age 60, $1,983 at 65, or $2,138 at 70, offering retirees a stable income stream.

Recent trends show significant growth in the annuities market, with fixed-rate deferred annuities increasing by 16.3% and registered index-linked annuities growing by 41.7%. Monthly payouts have also risen, such as a 20.5% increase in payouts for a $100,000 annuity between 2022 and 2023.

Factors like age, gender, payout structure, and interest rates play a key role in determining annuity payouts. For instance, deferring payments to older ages can yield higher returns, with a 65-year-old man receiving $4,000 monthly by age 80.

When compared to other retirement options like Social Security, IRAs, pensions, and 401(k)s, annuities stand out for providing guaranteed lifetime income. As retirees face rising costs and longer lifespans, annuities remain a reliable and customizable option to secure financial stability in retirement.

Fair Use Statement

Readers can share these findings for noncommercial purposes only and must provide a link back to this page at RetirementLiving.com.

Sources

- How Much Does a $300,000 Annuity Pay per Month? Annuity.org. Evaluated January 20, 2025.

Link here - Jeannine, M. How much cash can a $300,000 annuity generate for me each month? AOL. Evaluated January 20, 2025.

Link here - Schell, J. A Record Number of Americans Purchased Annuities in 2023. Annuity.org. Evaluated January 20, 2025.

Link here - How Much Does a $300,000 Annuity Pay Per Month? Smart Asset. Evaluated January 20, 2025.

Link here - Annuity Calculator: How Much Do Annuities Pay Per Month? The Annuity Expert. Evaluated January 20, 2025.

Link here - How Much Does a $200,000 Annuity Pay per Month? Annuity.org. Evaluated January 20, 2025.

Link here - How Much Does A $100,000 Annuity Pay Per Month? Annuity.org. Evaluated January 20, 2025.

Link here

- How Much Does a $750,000 Annuity Pay Per Month? Annuity.org. Evaluated January 20, 2025.

Link here

- The case for life annuities. Investment Executive. Evaluated January 20, 2025.

Link here - Interest-rate hikes boost annuities sales, payouts. Investment Executive. Evaluated January 20, 2025.

Link here

- US annuities on track to have another record-breaking year in 2024. SP Global. Evaluated January 20, 2025.

Link here

- United States Fed Funds Interest Rate. Trading Economics. Evaluated January 20, 2025.

Link here

- Release: Quarterly Retirement Market Data, Third Quarter 2024. Investment Company Institute. Evaluated January 20, 2025.

Link here

- Pension vs. Annuity: What’s the Difference? Smart Asset. Evaluated January 20, 2025.

Link here

- Income from Pensions. Pension Rights Center. Evaluated January 20, 2025.

Link here

- Daugherty, G. 5 Key Changes to 401(k)s in 2025 and What They Mean for You. Investopedia. Evaluated January 20, 2025.

Link here

- Numbers Retirement Plan Sponsors Need to Know for 2025. Segal. Evaluated January 20, 2025.

Link here