Retirement Living takes an unbiased approach to our reviews. We may earn money when you click a partner link. Learn More

Best Annuities

Find the right annuity for steady, worry-free income in retirement.

Updated:

Annuities can provide steady, guaranteed income during your retirement. Learn about the different types of annuities, get tips for choosing one that will fit your needs, see answers to frequently asked questions, and explore our in-depth reviews of the top annuities companies.

4.6

Annuity Gator is an annuity marketplace that allows customers to compare annuities to find the best option. Independent annuity professionals provide honest advice, better products, and personalized products for your situation.

- Great marketplace

- Compare top annuities

- Low fees

Fidelity offers three classes of annuities. If you own an annuity and want to switch it to Fidelity, you can get a tax-free, low-fee exchange with their Personal Retirement Annuity.

- Great asset accumulation

- Affordable deferred fixed annuities

- Trade and rebalance without penalty

4.6

Gainbridge is a modern insurance agency that allows individuals to purchase annuities through a fully digital process. Customer support representatives are highly rated, licensed representatives available to help with any questions.

- Quick & simple process

- Provide up to 5.70% APY

- Fully digital application process

MassMutual has one of the best financial ratings in the industry. As well as being a life insurance company, It offers five types of annuities and is best for those who are new to annuities, especially in terms of how they work.

- Top financial strength rating

- High financial strength rating

- Live customer service representatives

4.6

Blueprint Income specializes in simple fixed and income annuities and delivers the best digital experience in the industry. Blueprint Income is appointed to sell products from more than 46 insurers. The company has a 4.3 out of 5.0 stars rating in Trustpilot and has an A+ on the Better Business Bureau (BBB).

- Great technology

- Fixed and income annuities

- Easily compare annuity rates in real-time

Allianz

4.8

Allianz offers two types of annuities: fixed index annuities and registered index-linked annuities. Both offer investment growth opportunities based on index performance while limiting risk. You may purchase annuities up to the age of 85. Allianz scores an above-average rating from JD Power.

- Great for limiting risk

- Annuities available up to age 85

- Opportunity for protection from market downturns

Nationwide is an easy-to-use online annuity management system that offers five different types of annuities. It has a high JD Power ranking, and riders receive an enhanced death benefit.

- Great for death benefits

- High JD Power ranking

- Over 90 equities to choose from

Annuity Company Reviews

You can buy annuities directly from the insurance companies that issue them or from independent brokers, banks, and other financial groups. With over 40 major insurance firms issuing annuities and hundreds selling them, knowing where to start your search can be daunting. Luckily, we did the hard work for you. We researched 20 of the top annuity companies and narrowed our list to the top three. Our in-depth annuity analysis focuses on each company’s industry reputation, the variety of offerings like long-term investments, and other criteria. Check out our methodology section to learn more about how we made our top picks.

Annuity Gator Review

Great marketplace

|

Annuity Gator provides education on annuities to help you understand and make the best decision.

Annuity Gator scores an impressive five out of five stars from nearly 500 reviews. You can expect personalized options, full transparency, and simple, honest guidance. You won’t be subject to fancy jargon or high-pressure sales tactics.

To learn more, read our full Annuity Gator review.

Fidelity Annuities Review

Great asset accumulation

|

Founded in 1946, Fidelity is known as one of the world’s most successful retail investment services firms, known for many firsts in the industry. Fidelity was the first to offer a web-based wealth management platform and money market funds with check-writing features, and it was the first mutual fund company with a website.

Fidelity offers three classes of annuities:

- Asset Accumulation: Fidelity Personal Retirement Annuity (minimum investment $10,000) or Deferred Fixed Annuities (minimum investment $5000).

- Asset Protection: For transitioning into retirement, Fidelity’s Deferred Income Annuities (minimum investment $10,000) and New York Life Clear Income Fixed Annuity – FP Series (minimum investment $50,000) are worth considering.

- Income Generation: If you’re already living in retirement and want to ensure you don’t outlive your money, Fidelity offers Immediate Fixed Income Annuities (minimum investment $10,000).

To learn more, read our full Fidelity Annuities review.

MassMutual Annuities Review

Top financial strength rating

|

With over 170 years of insurance products and investment experience, MassMutual has one of the best ratings in the industry. Respected financial strength rating companies give MassMutual high marks. A.M. Best posts a superior A++ rating, Moody’s rating is Aa3 (high quality), and Standard & Poor’s rank is AA+ or very strong.

MassMutual offers five different types of annuities:

- Deferred Fixed Annuity: This option has a guaranteed fixed interest rate, tax-deferred growth, and principal protection.

- Variable Annuity: This annuity option has tax-deferred growth potential and a range of investment choices, but has the potential for loss in value.

- Fixed-Index Annuity: This option has tax-deferred growth, or if you elect the guaranteed lifetime withdrawal benefit, you can meet predictable income goals.

- Immediate Income Annuity: As the name suggests, this option is best for those with immediate income needs. Guaranteed income starts within 13 months of the issued contract.

- Deferred Income Annuity (DIA): This option is best for future income needs.

To learn more, read our full MassMutual Annuities review.

What Is An Annuity?

If you’re new to annuities, start with knowing what this type of investment is: cash invested as a lump sum to produce a monthly income stream for life or a fixed period. The monthly income starts right away if you buy an immediate annuity or, in the future, if you buy a deferred annuity. A deferred annuity provides a more substantial payout than an immediate annuity since the backing insurance company has more time to invest your funds. Pension funds are annuities, although this retirement benefit is rarely offered by employers anymore. Social Security is another example of how annuities work.

Annuity Types

There are two main types of annuities: Deferred and Immediate. Within these two main categories, your annuity can either be fixed or variable, depending on whether your payout is a fixed sum tethered to the market’s overall performance, a group of investments, or a combination of the two.

- Deferred Annuity – If you choose a deferred annuity, your money is invested for a predetermined period of time until you hit retirement and are ready to start making withdrawals.

- Immediate Annuity – With an immediate annuity, you’ll start getting payments sooner after you’ve made your initial investment. Immediate annuities are good for people approaching retirement age.

Another way to look at the two is that a Deferred annuity accumulates money over time, while an Immediate annuity pays out quickly.

Who Should Invest In An Annuity?

Annuities are best suited to those who have maxed out tax-deferred contributions to 401(k) plans and IRA plans. The Internal Revenue Service (IRS) defines the maximum allowable contributions to pretax 401(k) and profit-sharing plans and both Roth and traditional IRAs. According to the Insurance Information Institute, there are no limits on the amount that you can invest in an annuity.

IRA and 401(k) accounts have hardship withdrawal or loan features if you need money for medical care, education, and some other expenses. An annuity is not as flexible; once you make a deposit, the contract locks into a surrender period of two to over 10 years. You will pay fees and a tax penalty if you withdraw any money.

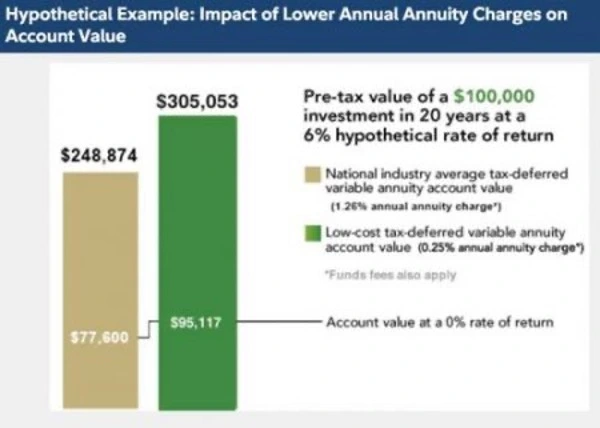

Annuities carry annual fees, transfer fees, expense risk charges, and other fees. Investor.gov explains more about annuity fees with information from the Security and Exchange Commission (SEC). Be prepared to compare the expenses of retirement accounts or see an independent financial planner for guidance.

There are a few types of annuities, like tax-sheltered, single life, or joint. Low-cost fixed or variable annuities are often the best option as a part of a retirement portfolio. Monthly payments will fluctuate with a variable annuity, while fixed annuities pay one monthly amount. No annuity is protected or insured, but they are considered safe investments.

Annuities Planning. Source: Getty

Annuities And Income Taxes

The main upside to annuities is that they guarantee an income stream and are safe investments. You pay no income taxes until you start to receive payouts in retirement, when your income should be lower. If you use pretax dollars from an existing IRA or 401(k) to buy an annuity, the payout will be fully taxed. If you buy an annuity with after-tax dollars, you will not pay taxes on the payout portion of your original investment, only the gains. Taxes are assessed at the regular income rate, not the capital gains rate.

The downside to annuities is that they are elaborate financial products with various fees and costs. You should seek professional assistance to help you choose the type that works best with your retirement portfolio and understand future tax implications.

When to Invest In An Annuity

Experts will tell you an annuity is not the first or even second retirement investment you should make. Max out other retirement savings accounts that offer tax-deferral or contribution matching. As a general rule, you should be investing 15 percent of your gross income in these accounts before you consider an annuity. To determine eligibility for Roth and traditional IRAs, see the IRS retirement plan rules.

| 1. Employer Plan with Matching | If your employer matches contribution to a 401(k) or 403(b) or other employer plans, contribute up to the maximum matching. |

| 2. Roth IRAs | Contribute to a Roth IRA with after-tax income (withdrawals are tax-free after the age of 59½). First, determine if you are eligible for a Roth. If you’re not eligible, skip to the next option. |

| 3. Employer Plan | Contribute the maximum allowed for the remainder non-matched portion of your employer-based plan. |

| 4. Traditional IRAs | Withdrawals will be taxed at a lower rate since your retirement income will likely go down. |

| 5. Annuity | Contribute to a tax-deferred annuity. You can invest in an annuity within an IRA if you prefer. |

Tips for a Wise Annuity Buyer

Investing a lump sum with one of our best annuity companies today will lead to a steady monthly cash stream in the future. As with any investment, it is essential to be informed and to understand the costs and the income. Wise investors research the market, annuity companies, types of annuities available, benefits and risks, and fees and commissions. The ins and outs of some annuities are so intricate that even the most seasoned investor can find themselves scratching their head, wondering what the best choice is. The following are some tips to keep in mind:

Top tips:

- If you buy an annuity when interest rates are low, you’ll get less value overall. Wait to buy until rates increase.

- You can transfer all or a portion of your 401(k) or IRA into an annuity.

- Look for and pay attention to words like “surrender charges” and “withdrawal rates” in the contract.

Methodology

We researched the top 20 annuity companies for seniors to invest in and narrowed the list to our top three. When you invest, you want benefits now and benefits down the road. After extensive research of government and consumer information on wise investing, we came up with a list of specific criteria for maximizing your benefits in both cases. The following is what we looked for when reviewing annuity products:

- Independent ratings

- Benefits and fees

- Commissions

- Financial health of the insurance companies that back the annuities

Based on this criteria, we chose the best three annuities companies. Each stands out above the competition.

FAQs

According to the IRS, the maximum 401(k) contribution in 2024 for employees who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan is $23,000. The contribution limit for IRAs for 2024 is $7,000, or up to $8,000 if you’re 50 or older. Since deferred annuities have no IRS contribution limits, you can invest as much as you want for retirement as a tax-deferred investment.

The two phases of annuities are the accumulation phase and the distribution phase. During the accumulation phase, you put money into the annuity with a lump sum, monthly payments, or a combination of the two. Your investment grows during this phase. The distribution phase, or annuity or annuitization phase, is when you start receiving payments from your investment.

The surrender period is the length of time an investor has to wait to withdraw funds from an annuity without incurring some fees or income tax penalties. Depending on the contract terms, this can be years.

What happens to an annuity after the owner’s death depends on several factors. The first and most important is whether or not the owner has a rider that allows the selection of a beneficiary or death benefit clause. With the clause, the beneficiary (or beneficiaries) will have three ways to receive payments after the owner’s death:

→ Lump Sum Distribution: Beneficiaries receive the funds as a lump sum amount.

→ Non-Qualified Stretch: Beneficiaries receive minimum payments stretched over their life expectancies.

→ Five-Year Rule: Beneficiaries can withdraw amounts during a five-year period or withdraw the entire sum in the fifth year.

Without the clause, the funds revert to the insurance company.

Once you determine that an annuity is a sound idea for your retirement portfolio, the earlier you buy into a deferred annuity contract, the higher the monthly income stream will be. A difference of 10 years between making a lump sum investment into an annuity can mean a difference of hundreds of dollars a month in income.

Conclusion

Do your homework before investing in an annuity, and take the time to read plan documents and ask questions until you understand how the annuity you’re considering works. You will need to know how much the investment will cost in fees and possibly penalties and how much you can expect to receive once you retire.

Annuities are an investment option that can work well but are inappropriate for all retirement savings plans. Creating a tailored investment plan for you and your family is never “one size fits all” and should be methodically planned out with the advice of professionals.

The Best Annuity Companies

- Great marketplace – Annuity Gator

- Great asset accumulation – Fidelity Annuities

- Quick & simple process – Gainbridge

- Top financial strength rating – MassMutual Annuities

- Great technology – Blueprint Income

- Great for limiting risk – Allianz

- Great for death benefits – Nationwide Annuities