Cost of Long-term Care Insurance by Age

Updated:

Open Access

About 70% of people aged 65 and older will need long-term care. A private room in a nursing home now costs over $116,000 per year. The cost of long-term care insurance by age varies widely.

A 55-year-old man pays about $950 per year, while a 65-year-old pays about $1,700 for the same coverage. Buying earlier locks in lower rates.

Key Insights

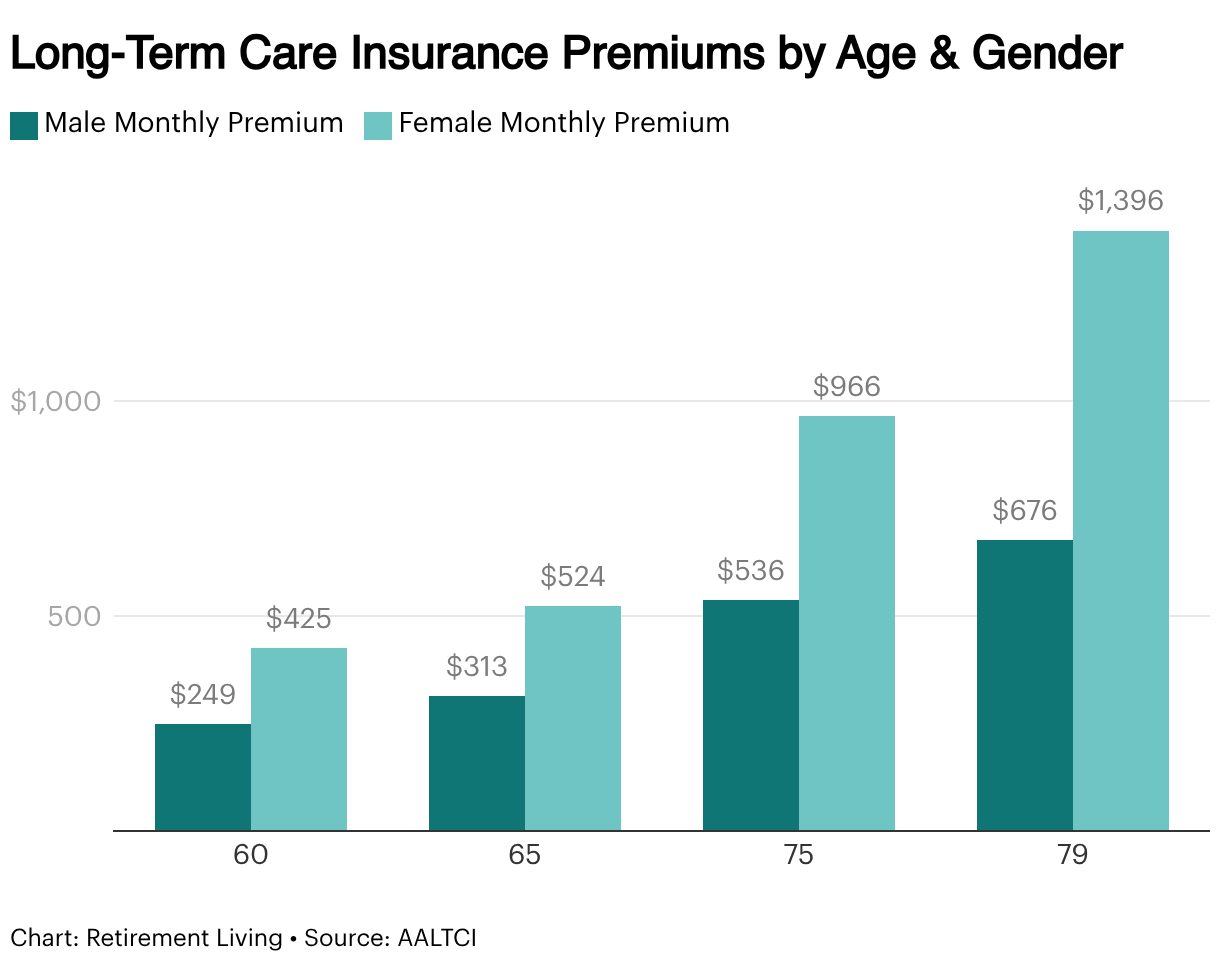

Monthly premiums rise sharply with age, increasing from $249 at 60 to $676 by age 79 for men.

↓ Jump to insight

Women pay significantly higher premiums than men at every age, with costs reaching $1,396 per month by age 79.

↓ Jump to insight

Eligibility declines with age, as denial rates increase from 12% in your 40s to 47% after age 70.

↓ Jump to insight

Long-term care costs without insurance exceed $75,504 per year for home care and $116,000 for nursing home care.

↓ Jump to insight

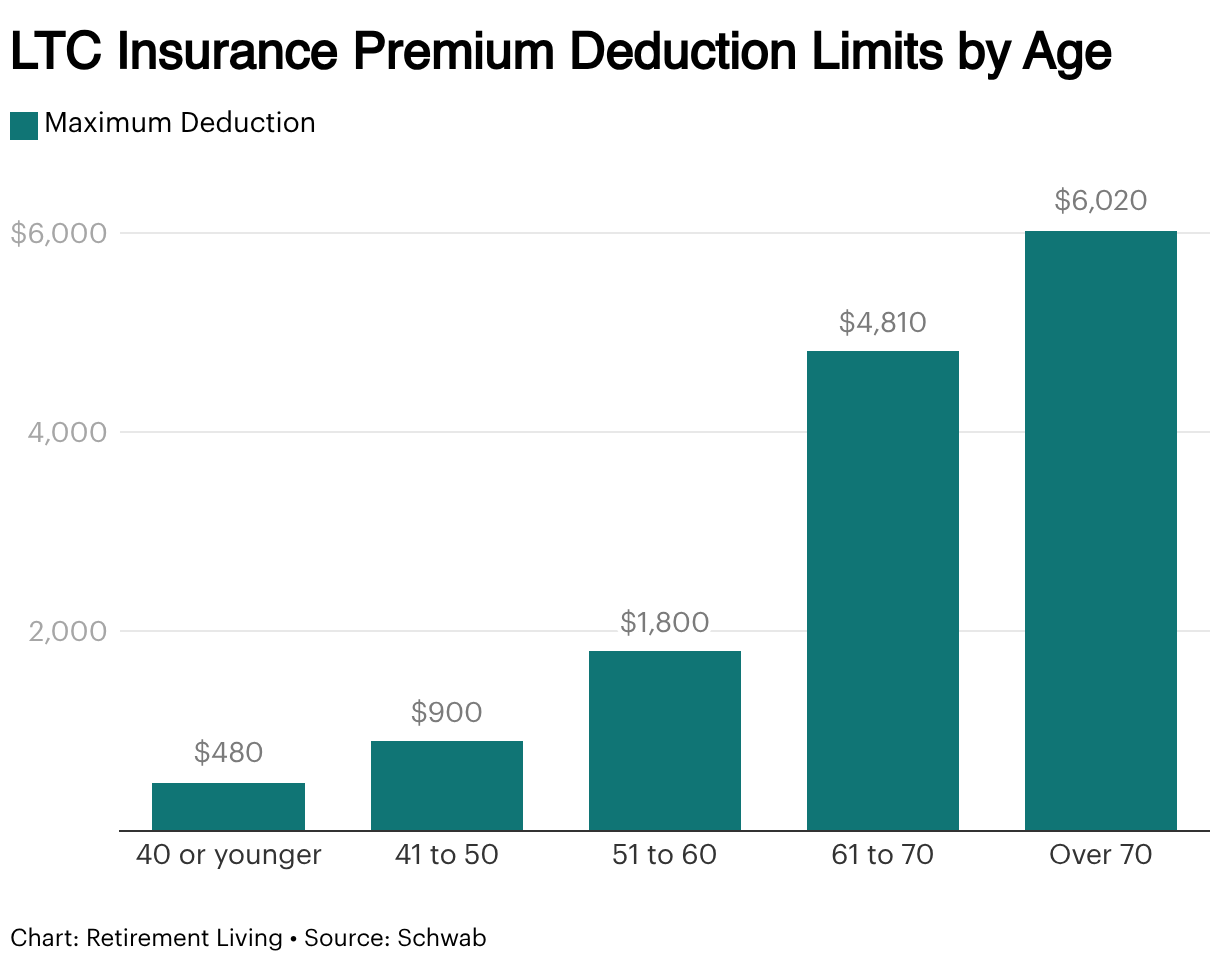

Tax deduction limits increase with age, rising to $6,020 annually after age 70.

↓ Jump to insight

Average Cost of Long-Term Care Insurance by Age

The average cost of long-term care insurance depends on your age at purchase. A standard policy includes a $165,000 benefit amount. Younger applicants pay lower annual premiums, while costs rise with age.

At age 55, a single male pays about $950 per year. A single female pays about $1,500 for the same coverage. Adding inflation protection increases premiums. A 55-year-old male pays $1,750 with 2% growth and $3,685 with 5% growth. A female pays $2,815 and $6,400 for the same options.

Costs increase by age 60 and 65. At age 60, a single male pays about $1,200 per year, while a single female pays about $1,900 per year. At age 65, the annual premium rises to about $1,700 for men and $2,700 for women. These long-term care insurance premiums show a steady increase with age.

Cost of Long-Term Care by Gender and Health Status

Health status affects eligibility and long-term care insurance premiums. Insurance companies review medical history before issuing a policy.

Pre-existing conditions such as Alzheimer’s disease, diabetes, or heart disease reduce eligibility. Applicants with these conditions face higher premiums or may not qualify.

Alzheimer’s disease often leads to extended care needs. After diagnosis, men live about 5.7 years and women about 8 years. More than half of individuals move to a nursing home within five years.

Long-term care needs already average about three years. Chronic conditions can extend this duration and increase total costs.

What Long-Term Care Insurance Covers

Long-term care insurance covers services that support daily living and ongoing health care needs. About 90% of people who need long-term care receive services outside of nursing homes, often at home or in community settings.

Coverage includes nursing home care, including private room costs, and care in an assisted living facility. It also covers in-home care, where a home health aide provides support with daily tasks.

Most policies pay for help with activities of daily living such as bathing, dressing, eating, and mobility. The type of care covered depends on the policy, but most plans include both facility-based care and home care services.

Key Policy Features That Affect Cost

Here are the main policy design features that determine your long-term care insurance premiums and coverage.

Benefit Amount and Daily Benefit

The benefit amount is the total amount your long-term care insurance policy will pay, while the daily benefit sets how much it pays per day for care.

A typical policy includes around $165,000 in total long-term care benefits, but higher benefit amounts increase your annual premium. Policies with higher daily benefits are especially important if you expect to need care in a nursing home or assisted living facility, where costs are significantly higher than home care.

Benefit Period and Elimination Period

The benefit period determines how long your policy will pay for long-term care services. Many policies offer coverage for 2 to 5 years.

Long-term care needs often last about three years on average, but certain health issues, such as cognitive decline, can extend care for much longer. Choosing a longer benefit period increases premiums but provides more financial protection.

The elimination period, or the waiting period, is the time you must pay for care before your insurance coverage begins. Most policies use a 30-, 60-, or 90-day elimination period.

Here’s what you need to keep in mind:

- A longer elimination period → lower premiums

- A shorter elimination period → less out-of-pocket cost

Inflation Protection

Inflation protection increases your benefit amount over time to keep up with rising health care and long-term care costs.

This feature is especially important because the median cost of a private room in a nursing home exceeds $116,000 per year, and costs continue to rise. Without inflation protection, your coverage may not be enough to pay for future care.

Policies typically offer 2% to 5% annual growth. While this increases your annual premium, it helps preserve the value of your long-term care coverage over time.

Exclusions and Limitations

Every long-term care insurance policy includes exclusions and coverage limits that affect when and how benefits are paid.

Most policies require you to meet eligibility criteria, such as needing help with at least two activities of daily living or having a cognitive impairment, before benefits begin.

Other common limitations may include:

- Restrictions on certain pre-existing health issues

- Limits on specific types of care

- Maximum daily or lifetime benefit caps

Types of Long-Term Care Insurance Policies

Here are the main types of long-term care insurance policies, each with different costs, benefits, and payment structures.

- Traditional Policies: Require ongoing annual premiums and provide a set pool of long-term care benefits for services like home health care, assisted living, or nursing home care. These policies typically have lower upfront costs and flexible benefit amounts and benefit period options, but they are often “use it or lose it,” meaning there is no payout if care isn’t needed. Premiums may also increase over time.

- Hybrid Policies (Life Insurance + LTC Coverage): Combine long-term care insurance with life insurance, offering both care coverage and a guaranteed death benefit. If long-term care isn’t used, the policy still pays out to loved ones, providing added peace of mind. These policies usually have higher premiums than traditional plans but offer more predictable costs and dual benefits.

- Annuities With Long-Term Care Benefits: Fund long-term care through a large upfront payment, often $50,000 or more, creating a pool for future health care and long-term care services. These policies can help cover in-home care, caregivers, or facility costs while allowing funds to grow over time. They’re best suited for those who want structured insurance coverage without ongoing premium payments.

How Much Does Long-Term Care Cost Without Insurance?

Long-term care creates high out-of-pocket costs. The median cost for an in-home health aide is about $75,504 per year. A private room in a nursing home costs over $116,000 per year.

These costs can last for years. Many people need care for about three years, which can exceed $200,000 in total out-of-pocket spending.

Medicare does not cover most long-term care services. It does not pay for extended nursing home stays or ongoing help with daily activities. This leaves most costs paid out of pocket.

Medicaid covers long-term care, but only after strict income and asset limits. Many people must spend down savings before they qualify, which delays coverage and increases out-of-pocket costs.

Best Age to Buy Long-Term Care Insurance

The best age to buy long-term care insurance is typically between 50 and 65, when premiums are more affordable, and eligibility is higher. Waiting too long can significantly increase long-term care insurance premiums and limit your coverage options.

Costs begin to rise more quickly after age 60, with premiums increasing at a faster rate each year. By the late 70s, the cost of coverage had more than doubled, making it much harder to secure an affordable insurance plan.

Eligibility also declines with age. As health status changes, more applicants face denials or stricter underwriting requirements, especially after age 70. Certain health issues may make it difficult to qualify for a long-term care insurance policy at all.

Buying earlier means paying premiums for a longer period, but it helps lock in lower rates, improves eligibility, and provides more flexibility in choosing coverage. For many people, this tradeoff offers better long-term value and greater peace of mind for both themselves and their loved ones.

Tax Deductions for Long-Term Care Insurance Premiums

Tax deductions increase with age, which helps offset rising long-term care insurance premiums in later years.

How to Choose the Right Long-Term Care Insurance Plan

Choosing the right long-term care insurance plan depends on your budget, health status, and expected care needs. The right policy should balance cost, coverage, and flexibility.

Here’s how to choose the right one:

- Work With an Insurance Agent or Financial Advisor: An experienced insurance agent or financial advisor can help you compare policies from different insurers and develop a personalized care planning strategy. They can also explain complex features like inflation protection, elimination period, and benefit limits.

- Compare Insurance Coverage Carefully: Review what each policy actually covers, including in-home care, home health care, assisted living, and nursing home care. Pay close attention to the daily benefit, benefit period, and any exclusions that could limit your long-term care benefits.

- Understand Your Insurance Plan Options: Compare different types of insurance, including traditional LTC insurance, hybrid policies, and annuities. Consider how each option fits your financial goals, whether it includes a death benefit, and how much you may need to pay out of pocket over time.

Bottom Line

The cost of long-term care insurance rises with age, but timing also affects your options. Premiums vary by insurance company, and similar policies can differ by up to 26% annually.

Policy design also plays a major role in long-term value. For example, adding inflation protection can significantly increase future benefits. A policy purchased at age 55 with 5% growth can increase in value from $165,000 to over $679,000 in benefits by age 85, helping to offset rising long-term care costs.

Caregiving is another often overlooked factor. About 64% of people rely on family members or friends for care, and unpaid caregivers frequently provide 20 to 45 hours of care per week, creating both financial and emotional strain.

In addition, policy pricing and eligibility depend heavily on health and timing. Waiting too long can limit access to coverage, and some insurers may stop offering policies at older ages, reducing your available options.

Ultimately, long-term care insurance is about maintaining control over your care choices, protecting your savings, and reducing the burden on your loved ones.

Fair Use Statement

If you have practical insight or experience with long-term care insurance, care planning, or caregiving costs, you may share it with us at [email protected]. Any personal information shared will remain confidential.

Sources

- NCOA – 6 Potential Roadblocks to Getting Long-Term Care Insurance (Evaluated 26 March 2026)

Link Here - American Association for Long-Term Care Insurance – 2025 Long-Term Care Insurance Facts, Prices, Data, and Statistics Report (Evaluated 26 March 2026)

Link Here - Charles Schwab – Managing the Cost of Long-Term Care (Evaluated 26 March 2026)

Link Here - Mutual of Omaha – Long-Term Care Insurance Cost Calculator and Estimates (Evaluated 26 March 2026)

Link Here - Carolina Family Estate Planning – How Much Does Long-Term Care Insurance Cost in North Carolina? (Evaluated 26 March 2026)

Link Here - New York Life – What Is the Cost of Long-Term Care? (Evaluated 26 March 2026)

Link Here