Retirement Living takes an unbiased approach to our reviews. We may earn money when you click a partner link. Learn More

Is Social Security Income Taxable?

A breakdown of when Social Security benefits are taxable, how income thresholds work, and what retirees should know about federal and state rules.

Updated:

|

Expert Reviewed

At a glance:

- Social Security benefits may be taxed depending on your “provisional income,” which combines your taxable income with a portion of your Social Security benefits.

- Single filers with income above $25,000 and joint filers above $32,000 may owe federal taxes on up to 85% of their benefits, with additional state taxes applying in some states.

- Whether you pay taxes on Social Security depends on your total income level, filing status, and where you live, with some lower-income beneficiaries fully exempt.

There are nearly 67 million Americans who receive monthly Social Security benefits, but not all beneficiaries pay taxes on them. The Internal Revenue Service (IRS) will determine how much tax you’ll pay by calculating your “provisional income:” your taxable income plus 50% of your Social Security benefit.

Key Takeaway: How much tax you pay on your Social Security benefits, if any, depends on your taxable income. The Social Security Administration (SSA) requires you to pay Social Security taxes if your provisional income exceeds $25,000 as an individual or $32,000 as a joint filer—up to a certain amount. Depending on where you live, you may pay both federal and state taxes.

Great ongoing promotions

American Hartford Gold Group

- No buyback fees

- Up to $15,000 in FREE silver on qualified accounts

2023 Tax Income Limits on Social Security

The Internal Revenue Service (IRS) adjusts its limits for calculating tax liability on Social Security income. For the tax year 2023, these are:

| Filing Status | Provisional Income | Social Security Tax Rate |

|---|---|---|

| Single or Head of Household | Less than $25,000 | No Tax |

| Single or Head of Household | $25,000 – $34,000 | Up to 50% |

| Single or Head of Household | More than $34,000 | Up to 85% |

| Joint Filers | Less than $32,000 | No Tax |

| Joint Filers | $32,000 – $44,000 | Up to 50% |

| Joint Filers | More than $44,000 | Up to 85% |

What Is the Maximum Social Security Tax Limit?

The maximum annual taxable Social Security is $160,300 for the tax year 2023, up from $147,000 in 2022. Workers also pay a Social Security tax rate of 6.2%, which means that the most you’ll pay in Social Security taxes for 2023 is $9,932 ($160,200 x 6.2%). The SSA also notes no one is required to pay taxes on more than 85% of their Social Security benefits.

Are There Federal Taxes on Social Security Income?

The same federal taxes you pay on standard income also apply to Social Security income. Your federal Social Security tax bill depends on:

- Your marital status: Half (50%) of your Social Security benefits, plus distributions from retirement accounts, earnings, investment income and pensions payments.

- Your annual provisional income: Married people have higher limits than single people.

If you file taxes as an individual and earned more than $25,000 in 2023, half of your social security income will be taxed up to 50%, But if you earned more than 34,000 in 2023, you’ll income will be taxed at a rate of up to 85%—which is the maximum amount.

Example: Let’s say you file individually, have $40,000 in income, and get $18,000 from Social Security each year ($1,200 a month). In this instance, you would pay taxes on 85% of your annual benefits, or $15,300. Under the SSA’s 6.2% tax rate, you’d pay about $9,486.

Determining the federal taxes on Social Security income can be tricky, but the IRS offers a worksheet you can use to calculate your taxes. You can also use tax software on any desktop computer, laptop or mobile device.

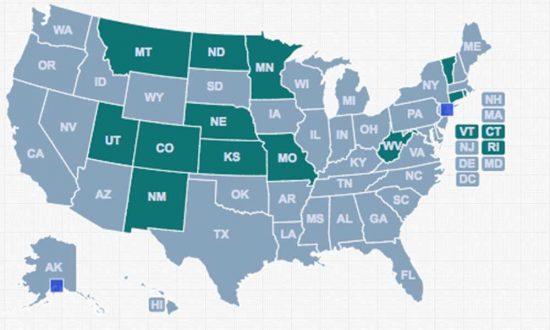

Are There State Taxes on Social Security Benefits?

The states that tax Social Security benefits are:

- Colorado

- Connecticut

- Kansas

- Minnesota

- Missouri (through tax year 2023)

- Montana

- Nebraska (through tax year 2023)

- New Mexico (most seniors are exempt)

- North Dakota

- Rhode Island

- Utah

- Vermont

- West Virginia (phasing out through 2026)

Check your state’s Department of Revenue website to find out how your state handles Social Security benefits. In most instances, states offer exemptions for at least a portion of Social Security income. If Social Security is your only source of income, you may be exempt from the tax.

Who Is Exempt From Paying Taxes on Social Security?

There is a small minority of people who don’t pay taxes on social security at all because their earnings are lower than the minimum provisional requirement. Single or head-of-household filers that earn less than $25,000 are exempt, as are joint filers with less than $32,000 in provisional income. On the other end of the spectrum, high-income individuals don’t have to pay Social Security taxes on earnings over $160,200 in 2023.

In addition, individuals are exempt from Social Security taxes if they meet the following criteria:

- Self-employed workers who make less than $400 annually

- Non-resident aliens, depending on visa type

- Certain religious groups

- Some foreign government workers

- Students working at their university (temporary exemption)

If you believe you may fall into one of these groups, consult your tax advisor or a financial advisor to ensure you file your federal and state tax returns correctly and avoid potential tax penalties.

Tax Filing Tips

IRS.gov has tax filing guidance, answers to frequently asked questions and an Interactive Tax Assistant to answer your tax law questions.

But there are several other ways to simplify the tax filing process, such as:

- Paying your taxes throughout the year. If you are worried about a large tax bill at the end of the year, you can make tax payments on your Social Security income throughout the year. To do so, you must fill out IRS Form W-4V to ask the SSA to withhold taxes from your Social Security benefits check, or you can pay quarterly estimates.

- Taking advantage of a free tax return preparation program. The IRS Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE) programs provide free tax help. VITA is available to people who earn $54,000 or less annually, people with disabilities and limited English-speaking taxpayers who need assistance with their tax returns. United Way can point you to your nearest VITA site. Comparatively, TCE provides free tax help for all taxpayers, including those 60 years of age and older. TCE also provides access to IRS-certified volunteers specializing in pensions and retirement-related issues.

- Consulting a professional. You can never be too careful or cautious when filing taxes and managing your Social Security. Consider hiring a qualified tax advisor, like a certified public accountant (CPA), for situation-specific assistance. You can also conduct regular check-in calls with your financial advisor to ensure your investments keep pace with your income and other retirement benefits.

From Our RICP® & CES™

“I often advise my clients that there isn’t a one-size-fits-all solution for everyone’s taxes. Each individual’s situation is unique. For some who typically owe taxes annually, paying early might be a viable option—but proceed with caution as the full picture emerges only at year-end. Planning ahead can be beneficial, enabling adjustments throughout the year with the assistance of a proactive tax professional who can provide estimates and projections.”

Christopher Hensley, RICP®, CES™

Financial Advisor

Bottom Line on Social Security Income and Taxes

Let’s face it: filing your taxes can sometimes be a long, arduous process, especially for those who need to account for Social Security income. Take time to understand your Social Security income—and how it relates to federal and state tax laws—so you can avoid costly, time-intensive filing mistakes.