How Much Would a Million Dollar Life Insurance Policy Cost?

Updated:

Open Access

A million-dollar policy can offer your family long-term financial security, but how much does it cost?

For a healthy 30-year-old, a million-dollar life insurance policy may cost around $48–$61 per month.

Key Insights

A healthy 30-year-old can expect to pay $48 to $61 per month for a $1 million policy.

↓ Jump to insight

At age 50, premiums increase from $167 to $234 per month for the same policy.

↓ Jump to insight

Smokers may face premiums 50-100% higher due to the increased risk of early mortality.

↓ Jump to insight

Individuals earning $100,000+ per year are often advised to have life insurance coverage 10-15 times their income.

↓ Jump to insight

The average U.S. mortgage debt stands at $148,222, and a $1 million life insurance policy can cover this debt and provide extra financial support.

↓ Jump to insight

What Does a One-Million-Dollar Life Insurance Policy Mean?

When people mention a one-million-dollar life insurance policy, they’re talking about the death benefit, the amount paid to your beneficiaries if you pass away while the policy is active.

This payout is income tax-free and typically given as a lump sum, though beneficiaries can opt to receive it in installments over time. This financial protection ensures your loved ones have the resources they need to cover expenses, debts, or future financial goals.

Factors That Affect the Cost of a Million-Dollar Life Insurance Policy

When considering a $1 million whole life insurance policy, understanding the key factors that influence its cost is crucial. Several elements determine how much you’ll pay in premiums.

Age and Health Status

Insurance companies assess the risk of insuring you based on how likely you are to pass away within a given timeframe. The younger and healthier you are, the lower your premiums will be.

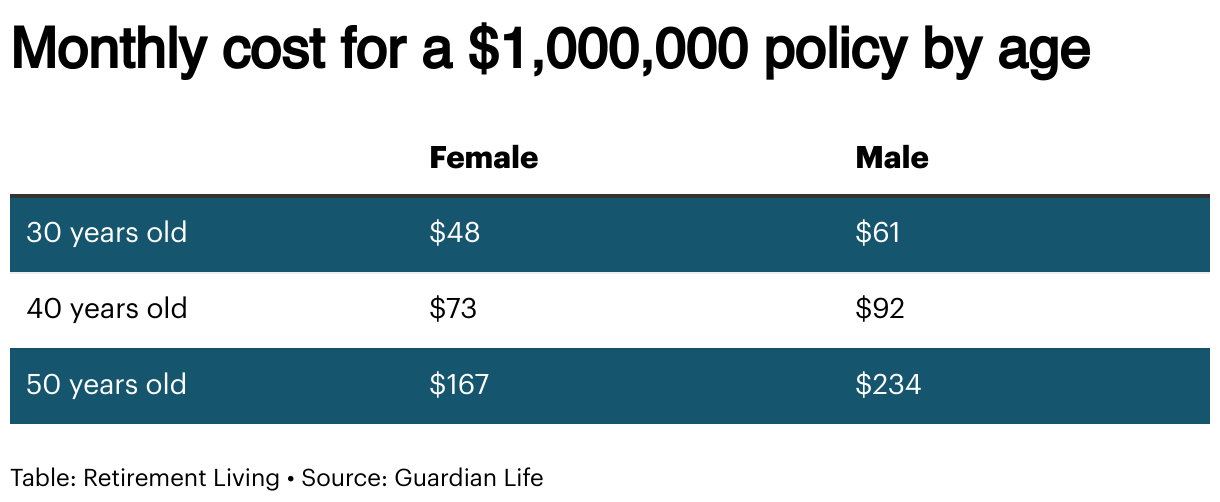

- Age: The younger you are when you buy a whole life policy, the more affordable your premiums will be. This is because insurance companies assume that younger individuals are less likely to pass away in the near term. For example, a 30-year-old in good health could expect to pay around $48 to $61 per month for a $1 million whole life policy. However, a 50-year-old could pay $167 to $234 per month, depending on health and lifestyle factors. Below is the Monthly cost for a $1,000,000 policy by age for a 20-year term life policy

- Health: Insurers will also take your medical history and lifestyle into account, often requiring a medical exam. If you’re in good health, you’re more likely to secure lower premiums. On the other hand, if you have chronic health conditions (such as diabetes or heart disease), your premiums could increase significantly. A smoker could see their premiums rise by as much as 50% to 100% due to the higher risk of early mortality.

Gender

Gender plays a role in determining life insurance premiums, as women statistically live longer than men. Mortality tables show that women tend to outlive men by about 5-7 years on average. This longevity impacts the premium costs.

A 30-year-old female might pay around $48 per month for a 20-year term life policy with a $1 million death benefit, while a 30-year-old male may pay about $61 per month for the same coverage.

Coverage Amount and Policy Type

The amount of coverage directly affects the cost. A $1 million policy costs more than a $500,000 one, so balance your needs with your budget. The type of policy you choose also impacts the price.

- Traditional Whole Life: Offers lifetime coverage and a guaranteed death benefit. Premiums are higher because they provide lifelong protection and slow-growing cash value, making it a long-term financial asset.

- Overfunded Life Insurance: Requires higher initial premiums but grows cash value faster. You can access this value through loans or withdrawals, making it both insurance and investment.

The type of policy you choose depends on your goals. If you’re looking for long-term coverage with the potential to build cash value, an overfunded policy might be the way to go.

However, if you just want lifelong protection without a focus on growing your cash value, a life insurance policy could be more suitable for you.

For those who prefer more affordable premiums with coverage over a fixed period, a 10-year term life insurance policy can offer a practical solution for shorter-term financial security without the complexity of building cash value.

Payment Frequency and Duration

How you pay for your life insurance can affect its cost. Paying annually often saves you 5-10% compared to monthly payments due to processing fees.

A rule of thumb is that some policies offer limited payment options (like 10-pay or 20-pay), where you pay premiums for a set number of years.

These can have higher annual premiums but let you fully own the policy sooner. If you can pay upfront, annual payments are usually the most cost-effective.

Dividends and Company Performance

Some whole life policies offer dividends (though not guaranteed). These can reduce premiums, buy extra coverage, or grow as cash value.

The financial strength of the insurance company matters, too. Strong companies with good ratings often offer better dividends and reliable cash growth.

Average Cost Estimates for a Million-Dollar Policy

The cost of a $1 million policy varies based on the term length and other factors like your age and gender.

Below are the average monthly premiums for a healthy, non-smoker 30-year-old male and female:

The longer your coverage term, the higher your monthly premium will be because the risk of death increases over time, making it more expensive to insure you for longer periods.

While 30-year term policies are pricier, they may be a good choice if you want protection for the long haul. Short-term policies (like 10 or 20 years) may seem more affordable, but they can end up costing you more in the long run if you need to get a new policy later, especially if your health declines.

An alternative to term life is permanent whole life insurance. It offers coverage for your entire life with fixed premiums that never increase, making it a solid option if you want peace of mind without worrying about rising rates.

Who Needs a Million-Dollar Life Insurance Policy?

A million-dollar life insurance policy can be essential for those whose family’s financial future would be significantly impacted by their loss. This level of coverage ensures that your loved ones are taken care of, no matter what life throws their way. Here are some common scenarios where this policy makes a lot of sense:

- High-Income Earners: If you earn $100,000 or more per year, experts typically recommend life insurance coverage of 10-15 times your income. A million-dollar policy can provide financial support to replace lost income and ensure your family can maintain their current lifestyle.

- Homeowners with Mortgages: If your family depends on your income to pay the mortgage, life insurance can protect them from the risk of foreclosure. With the average U.S. mortgage debt at about $148,222, a million-dollar policy can cover that debt and provide extra financial support for daily expenses, ensuring your family stays in their home without the financial strain.

- Parents of Young Children: Raising kids is expensive. A study showed that middle-income parents will spend an average of $310,605 to raise a child born in 2015 until they turn 17. A million-dollar life insurance policy can help cover those costs, from daily needs to education, college tuition, financial needs, and living expenses, ensuring your children’s future is secure, even if you’re not there to provide for them.

- Stay-at-home parents: The value of stay-at-home parents goes beyond the paycheck. Life insurance can help cover the cost of childcare, home management, daily support, and even student loans.

- Business Owners: For entrepreneurs or key members of a business, a 1-million-dollar policy can protect against business disruption and cover final expenses. In fact, more than 50% of new businesses in the U.S. fail within the first 5 years. A solid life insurance policy can ensure business continuity, cover any outstanding debts, and protect against financial setbacks.

- Individuals with large debts or dependents: If you have co-signed loans, debts, or dependents like aging parents or a special-needs child, this policy ensures those financial obligations are met.

- High-net-worth individuals: A million-dollar policy can offset estate taxes, provide liquidity for heirs, assist in wealth transfer and legacy planning, and replace an annual salary for your family’s financial security.

Bottom Line

A $1 million life insurance policy can cost $48 to $61 per month for a healthy 30-year-old, but premiums can rise to $167 to $234 per month at age 50. Smokers may face premiums 50-100% higher due to increased risk. With premiums influenced by age, health, and policy type, it’s important to consider your individual situation to ensure you’re getting the right coverage for long-term financial security.

Fair Use Statement

You’re welcome to share this insightful article for noncommercial purposes, but please link back to this page at RetirementLiving.com.

Sources

- Guardian Life. Million Dollar Life Insurance Policy. Guardian Life. Evaluated Feb. 18, 2025.

Link Here. - Top Whole Life. 5 Factors That Affect the Cost of a $1 Million Whole Life Insurance Policy. Top Whole Life. Evaluated Feb. 18, 2025.

Link Here. - Aditya Birla Capital. Why Are Life Insurance Premiums More Expensive for Smokers? Aditya Birla Capital. Evaluated Feb. 18, 2025.

Link Here. - Harvard Health. Why Men Often Die Earlier Than Women. Harvard Health. Published Feb. 19, 2016. Evaluated Feb. 18, 2025.

Link Here. - Bankrate. Who Needs a Million-Dollar Life Insurance Policy? Bankrate. Evaluated Feb. 18, 2025.

Link Here. - Statista. Life Insurance Statistics. Statista. Evaluated Feb. 18, 2025.

Link Here. - LendingTree. U.S. Mortgage Market Statistics. LendingTree. Evaluated Feb. 18, 2025.

Link Here. - U.S. Department of Agriculture. The Cost of Raising a Child. USDA. Evaluated Feb. 18, 2025.

Link Here. - Investopedia. The Cost of Raising a Child in America. Investopedia. Evaluated Feb. 18, 2025.

Link Here. - Business Dasher. Small Business Failure Statistics. Business Dasher. Evaluated Feb. 18, 2025.

Link Here.