Whole Life Insurance Rates by Age Chart: 2026 Key Stats

Updated:

Open Access

Life insurance costs rise with age, making early enrollment a smart financial move. As of September 2024, a term life policy averages $26 per month, while whole life coverage for the same amount can cost around $450. Premiums typically increase by 8% to 10% annually after age 40, meaning the longer you wait, the more you’ll pay. Locking in a policy early can save you thousands over time. Locking in a policy early can save you thousands over time, as the cost of whole life insurance at age 65 is significantly higher due to age-related pricing factors.

Key Insights

Whole life insurance rates rise by 8% to 10% annually after age 40, with increases reaching 12% per year for those over 50.

↓ Jump to insight

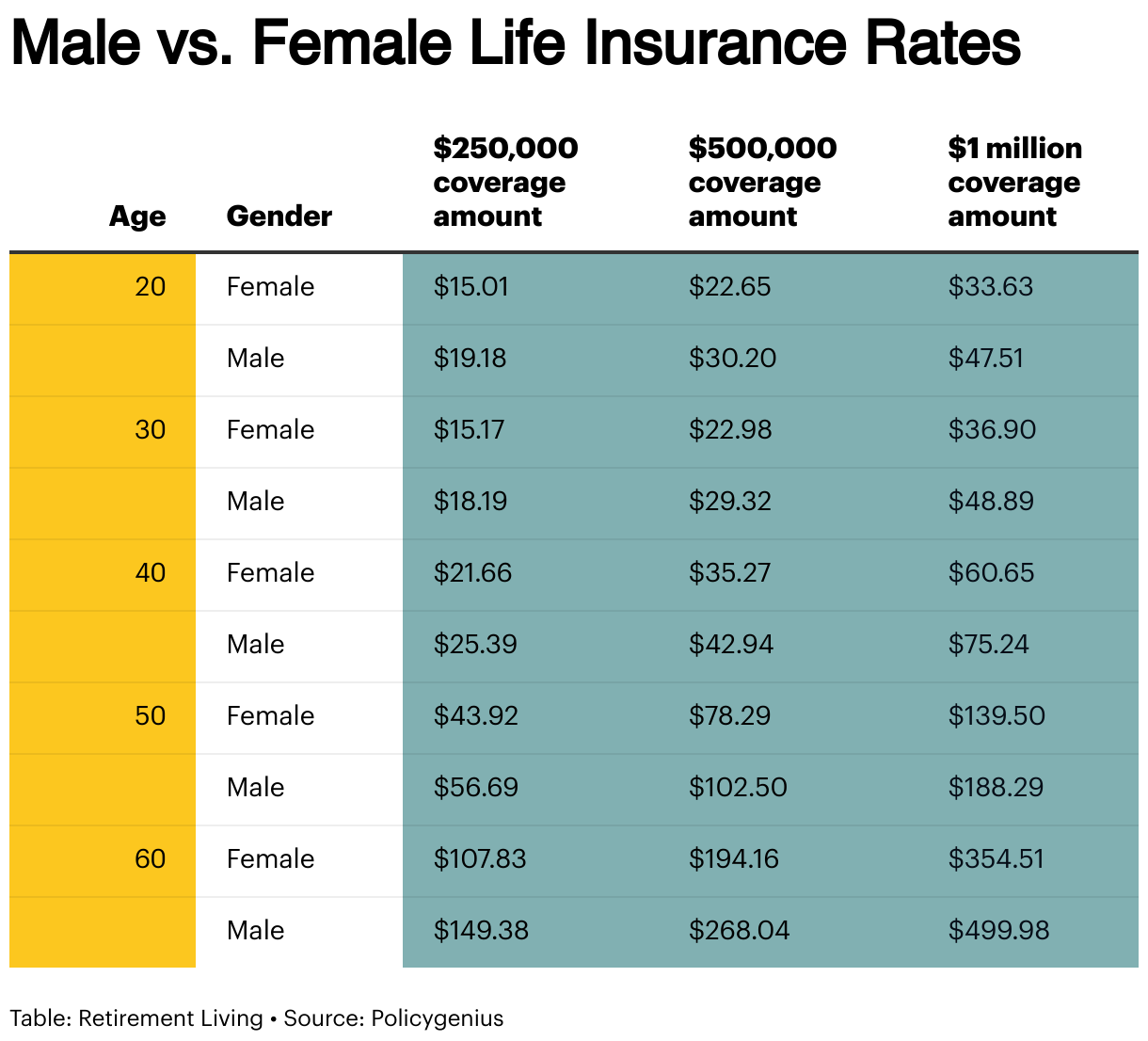

Women pay 24% less than men for the same whole life insurance coverage due to their longer life expectancy.

↓ Jump to insight

As of September 2024, the average monthly rate for term life insurance is $26, while whole life insurance costs around $450 per month for the same coverage.

↓ Jump to insight

Smokers pay 100% to 300% higher life insurance premiums than non-smokers due to increased health risks.

↓ Jump to insight

A $1 million life insurance policy costs significantly more than a $250,000 policy, with rates varying based on age, gender, and health history.

↓ Jump to insight

How Does Whole Life Insurance Work?

Whole life insurance is a permanent life insurance policy, meaning it provides coverage for your entire lifetime as long as you continue paying the premiums. Unlike term life insurance, which only lasts for a specific number of years, whole life insurance never expires.

One of the biggest advantages of a whole life insurance policy is that everything is guaranteed. Your premiums will never increase, no matter how long you have the policy.

The death benefit will never decrease, ensuring that your beneficiaries receive the full payout. Additionally, your policy cannot be canceled due to age, giving you lifelong peace of mind.

Another feature of whole life insurance is the cash value component. A portion of your premiums goes into this cash value, which grows over time. When you pass away, your beneficiaries receive the death benefit as a tax-free payout.

They can use this money for anything they need, whether it’s covering burial expenses, paying off medical bills, settling outstanding debts, or securing their financial future.

How Much Is Life Insurance?

Life insurance premiums vary based on the type of policy you choose. As of September 2024, the average monthly rate for a term life insurance policy is $26. For a 30-year-old male, a 20-year term policy with a $500,000 payout has a monthly premium of around $30, while a female of the same age pays about $23.

But if you opt for whole life insurance, the monthly premium jumps to around $450 for the same coverage. Mutual of Omaha is often the most affordable option for whole life coverage of $50,000 or less.

Factors Affecting Life Insurance Prices

Life insurance rates aren’t just based on age, gender, and the type of policy you choose. Life insurance companies also consider your health history, lifestyle, and coverage amount when determining your premium.

Here’s a closer look at what affects your costs.

Age

Age is the biggest factor for a life insurance policyholder. The older you are, the more you’ll pay, and in some cases, your age could even determine whether you qualify for coverage at all.

With whole life insurance, premiums increase every year. On average, they rise by 8% to 10% annually. However, the rate of increase varies:

- If you’re in your 40s, your premium may only increase by 5% per year.

- If you’re 50 or older, the annual increase can be as high as 12%.

This jump in pricing is especially noticeable after age 40 when rates start rising significantly.

That’s why it’s best to lock in coverage as early as possible. The younger you are when you buy, the lower your monthly payments will be.

Gender

Women generally pay less than men for the same policy. This is because women, on average, live longer than men, which means insurance companies view them as less risky.

Women pay, on average, 24% less than men for the same coverage.

Amount of Coverage

The more coverage you need, the higher your premiums will be. A $1 million policy will cost significantly more than a $250,000 policy. Insurance agents calculate premiums based on the risk they take on, so larger policies come with higher costs.

Health

Your health plays a crucial role in determining how much you’ll pay for life insurance. Insurers typically review your health history and medication use in two ways:

- Medical records database – A review of your medical history and past health records.

- Medical exam – Some policies require a health exam, though it’s possible to get life insurance without one.

Just like with health insurance, pre-existing conditions (like diabetes or heart disease) can increase your premium. During underwriting, insurers assess your health risks, so maintaining good health can help you secure lower rates.

Lifestyle

Insurance agents often assess activities that increase risk, such as extreme sports or risky hobbies. If you’re an avid skydiver, scuba diver, or frequent traveler, your life insurance plan could be higher than someone with a more typical lifestyle.

A poor driving record can also increase your life insurance rates. If you have a history of accidents or traffic violations, life insurance companies may consider you a higher risk and raise your final expense.

Smokers also typically pay higher rates for life insurance. Life insurance for smokers can be 100 to 300 times more expensive than for non-smokers. The health risks associated with smoking make insurers charge higher premiums to compensate for the increased likelihood of health issues or early death.

Type of Insurance

There are two main types of life insurance:

- Permanent life insurance – Includes whole life, universal life, and variable life. These policies provide lifetime coverage and build cash value over time. However, they generally come with higher premiums due to the lifelong coverage and savings component.

- Term life insurance – Offers coverage for a specific term (e.g., 10, 20, or 30 years). It’s typically more affordable than permanent life insurance, but it doesn’t build cash value.

The type of life insurance you choose directly impacts the cost of coverage, as permanent life policies tend to be more expensive due to their long-term benefits and cash value accumulation.

Bottom Line

Whole life insurance guarantees lifetime coverage, but it comes at a higher cost than term life insurance. Your age, gender, health, and lifestyle significantly impact how much you’ll pay.

Premiums rise by 8% to 10% per year after age 40, with women paying 24% less than men. Smokers pay 100% to 300% more, and a $1 million policy costs significantly more than a $250,000 policy.

The earlier you secure a policy, the more affordable your premiums will be. Understanding these factors and comparing rates will help you make an informed decision about which policy best protects your loved ones and fits your financial goals and needs.

Fair Use Statement

You’re welcome to share this insightful article for noncommercial purposes, but please link back to this page at RetirementLiving.com.

Sources

- Average Life Insurance Rates. Business Insider. Evaluated February 10, 2025.

Link Here - Do Whole Life Insurance Premiums Increase with Age? PolicyBachat. Evaluated February 10, 2025.

Link Here - Gender and Life Insurance Costs. Policygenius. Evaluated February 10, 2025.

Link Here - Average Life Insurance Rates. NerdWallet. Evaluated February 10, 2025.

Link Here - Whole Life Insurance Rates Chart. Choice Mutual. Evaluated February 10, 2025. Link Here