The Cost of Whole Life Insurance at Age 65: Key Statistics

Updated:

Open Access

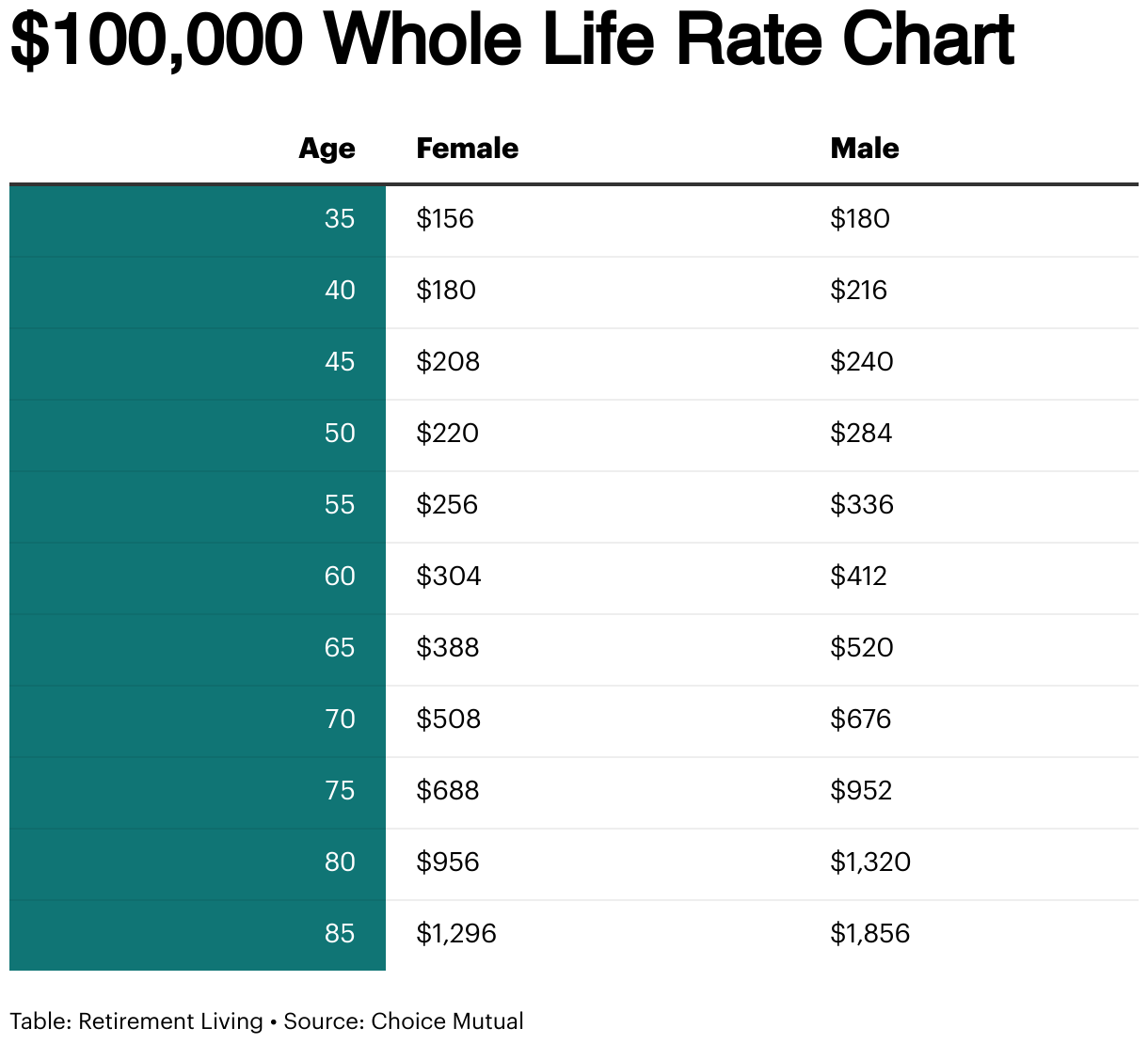

At age 65, whole life insurance premiums are significantly higher due to increased mortality risk. A healthy 65-year-old male might pay $520 per month for a $100,000 policy, compared to $180 per month at age 35.

Meanwhile, 70% of seniors will need long-term care, with women averaging 3.7 years of support. Understanding these costs helps retirees plan for financial security and healthcare needs.

Key Insights

A healthy 65-year-old male pays $520 per month for a $100,000 whole life policy, compared to $180 per month at age 35.

↓ Jump to insight

70% of seniors will need long-term care, with women requiring 3.7 years on average and men 2.2 years.

↓ Jump to insight

1 in 4 seniors will require long-term care for at least 5 years.

↓ Jump to insight

Long-term care costs can exceed $14,000 per month in some cities.

↓ Jump to insight

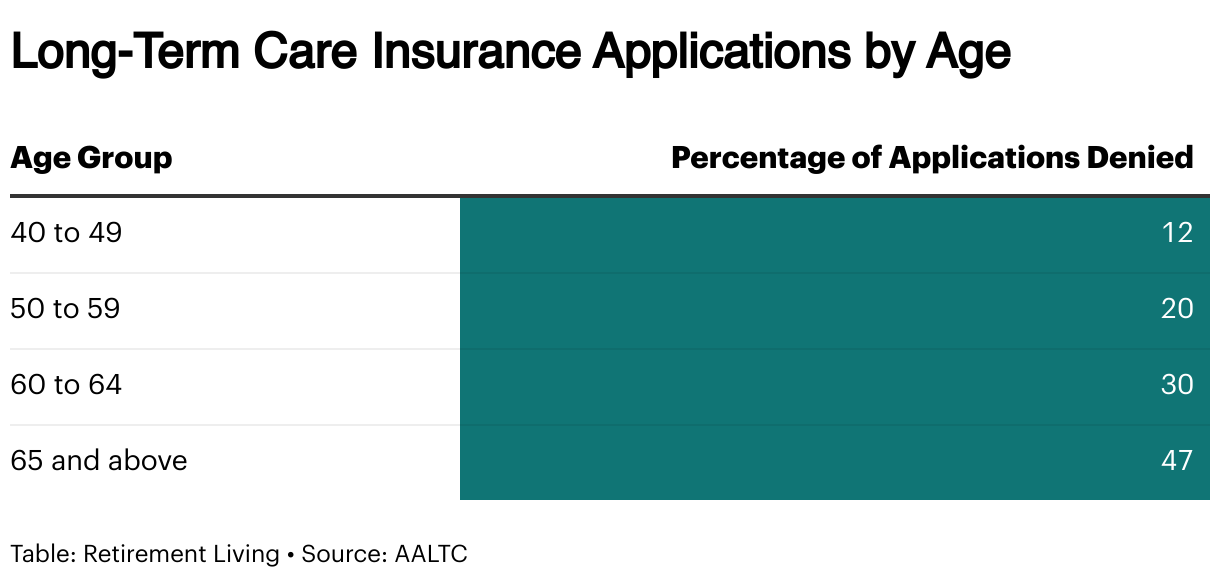

47% of long-term care insurance applications are denied for those aged 65 and above.

↓ Jump to insight

Understanding Whole Life Insurance

Whole life insurance provides lifetime coverage with fixed premiums and a guaranteed death benefit. Unlike term life insurance, which expires after a set period, whole life builds cash value over time, making it both a financial asset and a protection plan.

The table below shows how cash value accumulates for a $100,000 whole life policy with a fixed death benefit, assuming premiums of $1,178 per year starting at age 35 for a non-smoking male:

Average Cost of Whole Life Insurance at Age 65

The cost of whole life insurance at age 65 varies based on factors like health, gender, and coverage amount. Premiums are generally higher than term life insurance due to the lifetime coverage and cash value component. A million-dollar policy comes at a much higher premium based on individual risk factors.

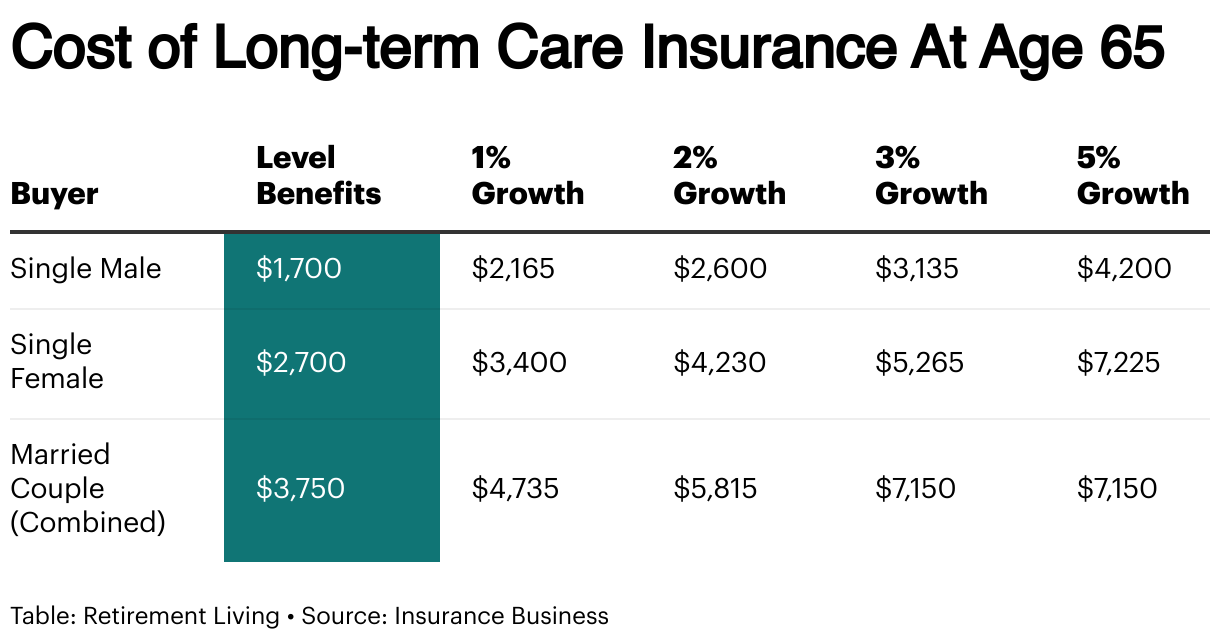

Many individuals at this age consider long-term care insurance to cover medical expenses later in life.

The table below outlines the average annual cost of long-term care insurance purchased at age 65, based on different benefit growth rates:

Since women tend to live longer, their premiums are higher. Couples often receive discounts when purchasing joint policies. Understanding these costs helps in planning for both life insurance and long-term care needs in retirement.

Key Factors Affecting Premium Rates

Several factors determine the cost of whole life insurance, including age, health, coverage amount, and policy type.

Understanding these can help you find the best rates.

Age and Health

At age 65, whole life insurance premiums are significantly higher due to increased mortality risk. For instance, a healthy 65-year-old male might pay approximately $520 per month for a $100,000 policy, whereas a 35-year-old male pays about $180 per month for the same coverage.

Policy Size

Premiums rise with higher coverage amounts. Larger policies require higher monthly payments, reflecting the increased payout obligation for the insurer.

Company-Specific Variations

Insurance providers set their own pricing based on underwriting criteria, financial stability, and risk assessment models. Comparing multiple quotes is crucial to finding the best rate.

Medical Underwriting & No-Exam Policies

Fully underwritten policies, which require a medical exam, tend to have lower premiums since insurers can accurately assess risk. No-exam policies, while more accessible, often come with higher costs to offset the unknown health risks.

Payment Structure and Riders

Some policies allow for limited pay options, where premiums are paid over a shorter period (e.g., 10 or 20 years) instead of a lifetime. This results in higher short-term costs but eliminates the need for payments in later years.

Adding riders, such as long-term care benefits or accelerated death benefits, can increase premiums but provide additional coverage flexibility.

Is 65 Too Old to Buy Long-Term Care Insurance?

Purchasing long-term care insurance at age 65 is still feasible, but it’s important to understand how age impacts both eligibility and premium costs. The older you are when applying, the higher your premiums will be.

Insurers may deny coverage based on health conditions that become more common with age, such as diabetes, heart disease, or cognitive impairments.

Many people delay purchasing long-term care insurance due to cost concerns, but waiting too long can result in higher premiums or ineligibility. Policies are typically more affordable and easier to qualify for at younger ages when applicants are in better health.

47% of long-term care insurance applications are denied for those aged 65 and above which is why early planning is essential.

The American Association for Long-Term Care Insurance (AALTCI) provides data illustrating how the age at which you apply can affect your premiums:

Is Whole Life Insurance Worth Having?

According to the Administration for Community Living (ACL), about 70% of Americans over 65 will require long-term care services at some point. Women, on average, need 3.7 years of care, while men require 2.2 years. Additionally, 1 in 4 seniors may need care for at least 5 years.

Without long-term care insurance, these expenses fall entirely on you and they can be overwhelming. Below are the 2023 average monthly costs for long-term care in three U.S. cities, based on the Genworth Cost of Care Survey:

Given these rising costs, having long-term care insurance can help protect your savings and ensure access to quality care when you need it most.

Bottom Line

Whole life insurance at 65 comes with higher premiums, but it provides lifelong coverage and cash value growth. A healthy 65-year-old male pays around $520 per month for a $100,000 policy, nearly three times more than at age 35.

At the same time, 70% of seniors will require long-term care, with women averaging 3.7 years of support. Costs for care can exceed $14,000 per month in some cities, making financial preparation crucial.

Whether through life insurance, long-term care policies, or a mix of both, securing coverage early can prevent financial strain and ensure peace of mind in retirement.

Fair Use Statement

You’re welcome to share this insightful article for noncommercial purposes, but please link back to this page at RetirementLiving.com.

Sources

- Investopedia. How Cash Value Builds in a Life Insurance Policy. Investopedia. Published Aug. 21, 2014. Evaluated Feb. 23, 2025.

Link Here - Choice Mutual. Whole Life Insurance Rates Chart. Choice Mutual. Evaluated Feb. 23, 2025.

Link Here - Insurance Business Magazine. Breaking Down Long-Term Care Insurance Costs by Age. Insurance Business Magazine. Evaluated Feb. 23, 2025.

Link Here - National Council on Aging (NCOA). How Much Does Long-Term Care Insurance Cost and Is It Worth It? NCOA. Evaluated Feb. 23, 2025.

Link Here