Retirement Living takes an unbiased approach to our reviews. We may earn money when you click a partner link. Learn More

What Do Medicare Supplement Plans Cover?

A breakdown of what Medicare Supplement (Medigap) plans cover, what they don’t, and how benefits vary by plan type.

Updated:

At a glance:

- Medicare Supplement (Medigap) plans help cover out-of-pocket costs like copays, coinsurance, and deductibles not paid by Original Medicare.

- Coverage varies by plan type (A–N), but most include hospital costs, skilled nursing coinsurance, and some emergency care abroad.

- Medigap does not cover services like dental, vision, hearing aids, or prescription drugs, which require separate coverage.

We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE (TTY users should call 1 (877) 486-2048) 24 hours a day/7 days a week to get information on all of your options.

With so many Medicare plans available, it’s hard to know what is (and is not) covered. If you purchase a Medicare supplement plan, it’ll help pay for gaps in your Medicare plan’s coverage. Let’s take a look at what Medicare supplement plans cover.

Medigap plans supplement, but do not replace, primary Medicare coverage. Fortunately, Medicare supplement plans are available from a variety of insurers to help pay for the following medical expenses:

- Coinsurance and hospital costs for up to one year after Medicare benefits are used up

- Blood transfusions for up to three pints of blood

- Hospice care coinsurance or copayment

- Skilled nursing facility care coinsurance

- Medicare Part A (hospital insurance) deductible

- Medicare Part B (medical insurance) deductible

- Part B excess charge (the difference between the amount a doctor or health care provider can legally charge and the Medicare-approved amount)

- Medical costs incurred while traveling outside of the U.S.

- Out-of-pocket limit

Costs Not Covered by Medicare Supplement Plans

A Medicare supplement plan is designed to fill in Medicare coverage gaps, but it does not account for all medical expenses. Typical medical costs not covered by a Medicare supplement plan include:

- Dental care, unless incurred during hospitalization

- Eye exams

- Eyeglasses

- Hearing aids

- Prescription drugs (plans sold after 2006)

Medicare Supplement Plans Coverage Explained

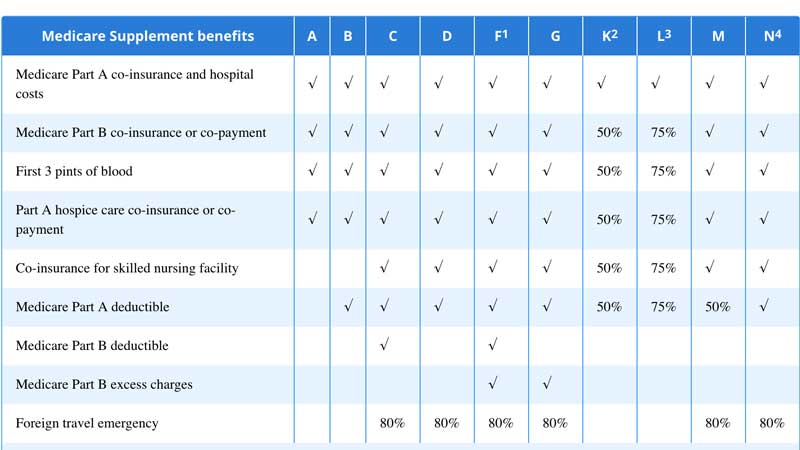

Medicare supplement plan benefits vary, but every plan provides coverage for coinsurance and hospital costs for up to one year after you’ve exhausted Medicare benefits. There are 10 Medicare supplement plans available in most states. (We discuss which states have different policies later in this article.)

- Plan A: Coverage for Part B coinsurance or copayment, blood transfusions, and hospice care coinsurance or copayment.

- Plan B: Includes the same coverages as plan A, along with Part A deductible coverage.

- Plan C: Same coverages as plan B, along with Part B deductible coverage and foreign travel coverage up to 80%. Plan C is being discontinued, and after Jan. 1, 2020, you will not be able to enroll in this plan.

- Plan D: Includes the same coverages as plan C, except Part B deductible coverage.

- Plan F: Same coverage as plan C, along with Part B excess charge coverage. Plan F is a high-deductible option, and enrollees must pay Medicare-covered costs up to $2,290 before their Medicare supplement insurance pays anything. Also, plan F is being discontinued, and after Jan. 1, 2020, you will not be able to sign up for this plan.

- Plan G: Mirrors plan F coverage, except Part B deductible coverage.

- Plan K: Plan K does not cover Part B deductibles, excess charges, and foreign travel exchanges, and it has an out-of-pocket limit of $6,620 in 2022 and $6,940 in 2023. It also covers up to 50% of the following costs:

- Part B coinsurance or copayment, blood transfusions

- Part A hospice care coinsurance or copayment

- Skilled nursing facility care coinsurance, and Part A deductibles

- Plan L: Plan L does not pay for Part B deductibles or excess charges, or foreign travel medical expenses, and it has an out-of-pocket limit of $3,130 in 2022 and $3,470 in 2023. It also includes coverage for up to 75% of the follo

- Plan M: Includes the same coverages as plan D, except 50% of Part A deductibles.

- Plan N: Includes the same coverages as plan A and 80% of foreign travel exchange coverage. It also covers 100% of Part B coinsurance or copayments, except for copayments of up to $20 for some office visits and up to $50 copayments for emergency room visits that don’t result in inpatient admissions. While four older Medicare supplement plans (E, H, I, and J) are no longer available, you can keep this coverage if you purchased one before June 1, 2010.

Medicare Supplement Plan Coverage Varies in Some States

Medicare supplement plans are available nationwide, but Massachusetts, Minnesota, and Wisconsin offer options differing from those available in other states.

Massachusetts

Core Medicare supplement coverage includes healthcare items and services under a health insurance plan, up to 60 days of inpatient time at a mental health hospital per calendar year, and various state-mandated benefits.

The core Massachusetts Medicare supplement plan does not cover Part A inpatient hospital deductibles, Part A skilled nursing facility coinsurance, Part B deductibles, or foreign travel emergencies. Monthly premiums for a Massachusetts Medicare supplement plan range from $113 to $341.

Minnesota

Basic and Extended Basic Medicare supplement plans are available to Minnesota residents. Minnesota’s core Medicare supplement coverage includes inpatient hospital care, medical costs, blood transfusions for up to three pints of blood annually, Part A hospice and respite care cost-sharing, and Parts A and B home health services and supplies cost-sharing. Annual premiums for Medicare supplement insurance in Minnesota range from $1,760 to $4,350.

Wisconsin

Core Medicare supplement coverage in Wisconsin consists of healthcare items and services under a health insurance plan, Part A skilled nursing facility coinsurance, and assorted state-mandated benefits. This coverage also provides up to 175 days per lifetime to supplement Medicare’s inpatient mental health coverage and up to 40 home health care visits in addition to those paid for by Medicare. Wisconsin Medicare supplement insurance annual rates average between $1,800 and $4,500.

The Bottom Line on Medicare Supplement Plans

Medicare supplement plans are ideal for those searching for ways to augment their Medicare coverage, but all plans differ quite a bit. It is crucial to examine each Medicare supplement option closely to choose the coverage that can serve you well for years.