Best Life Insurance Companies

Updated:

By: Dr. Steven Rydin

Director of Product

Edited By: Jeff Smith

Sr. Content Manager

Retirement Living takes an unbiased approach to our reviews. We may earn money when you click a partner link. Learn More

We evaluated 17 well-known life insurance companies, and after careful review identified today’s best life insurance providers.

TruStage Life Insurance

- Great Budget Options

- Policies to fit a budget

- Online purchase options

Trustage Life Insurance is great for those on a fixed budget. Customers provide their budget and Trustage searches for a life insurance policy to fit your budget.

- Great Comparison Shopping

- Trusted by more than 2 million families

- Dedicated agent

SelectQuote is an online independent insurance broker that helps consumers find the best life insurance options with price and policy comparisons.

ReliaQuote

- Great for term life policies

- High coverage amount

- Life insurance calculator

ReliaQuote has a life insurance calculator to help determine how much coverage you need. Sells term life policies only.

Fidelity Life Insurance

- Great Term Insurance

- 24-48 hour approval

- No exam necessary

Fidelity Life Insurance offers term life insurance with easy and affordable monthly rates. Choose from 10, 20, or 30 year terms with options with no exams.

Everyday Life Insurance

- Great for tailored quotes

- Term and whole life insurance

- Policies available up to age 85

Everyday Life Insurance leverages advanced technology to match you with the best policy for you. Most customers don’t need to take a medical exam and approval odds are 80%.

- Great For Healthy Individuals

- Considers your physical activity

- Personalized policies

Health IQ is one of the only life insurance companies that consider your current health, health literacy and physical activity to provide a personalized life insurance policy.

- Great Coverage

- Up to $500,000 coverage cap

- Simplified process

Haven Life Insurance has a goal to remove the hurdles and confusion of life insurance to help you find the best way to protect yourself and your family with term insurance.

- Great Policy Matching

- AI technology matching

- $100,000 to $5 million in coverage

Leap Life is a life insurance broker that uses Artificial Intelligence (AI) technology to match you with a policy yielding significant savings. Savings range from 40 to 300% and policies come with 10-, 15-, 20- and 30-year terms.

AIG Direct

- Great Reliability

- Customized policy quote

- Covers customers worldwide

AIG has provided life insurance coverage to millions of customers for nearly a century. Protect your family with a customized term life insurance policy.

AAA Life Insurance Company

- Great for guaranteed coverage

- Guaranteed coverage available up to $25,000

- Discounts for AAA members

AAA Life Insurance Company offers several policies designed to help cover final expenses or burial costs. The company has whole life policies ranging from $5,000 to $75,000, and term and universal policies up to $5 million.

- Great cost estimates

- Quotes from top-rated companies

- Speak to a licensed expert

Policygenius offers term and whole life insurance quotes to help you compare over 10 top-rated life insurance companies like Lincoln Financial, MassMutual and Pacific Life. Get a cost range estimate online.

- Great Service

- Helpful Agents

- Large network

State Farm has been in business since 1922 and has grown to provide 83 million policies and accounts. Along with various types of life insurance, State Farm offers personal policies to cover your home, vehicles, identity theft, disability insurance and more.

- Great Value

- A la carte style pricing

- Free Quote

The goal of Gerber Life Insurance is to help parents and older adults achieve financial security through life insurance policies that are affordable for both children and adults.

Compare Top Life Insurance Companies

We evaluated 17 well-known life insurance companies, and after careful review, identified today’s best life insurance providers. During our search, we analyzed consumer reviews, government data and industry insights.

In this guide, we’ll discuss life insurance, how it works and its benefits. We’ll also provide tips for making wise life insurance decisions, review the best companies in the industry and answer frequently asked questions. By doing so, we’ll provide you with a comprehensive life insurance guide to help you choose the best possible life insurance policy for your individual needs.

Top tips:

- Review term and cash value life insurance options

- Determine how much coverage you need

- Reassess your life insurance policy every 5 years

Tips for a Wise Life Insurance Buyer

If you’re looking for life insurance, you are probably trying to find a policy that delivers the right mix of customer support, affordability and protection. While there is no one-size-fits-all life insurance plan, before you choose a life insurance company, follow these guidelines to make a wise purchase.

Our Life Insurance Expert

Kim Butler is the author of the books Live Your Life Insurance and Busting the Financial Planning Lies. Founder of Partners for Prosperity, LLC, Kim Butler has shunned common financial products such as stocks, bonds, savings accounts and CDs in favor of alternative investments, private lending, and creative life insurance strategies outside of the typical financial planning “box.” “NOT YOUR TYPICAL FINANCIAL PLANNER. Financial services expert Steve Savant calls Kim Butler an ‘investment advisor and cultural contrarian… the matron of money, a Joan of Arc crusader separating financial fact from fiction.’” – iReport.cnn.com

Kim Butler, Prosperity Economics Advisor. Principal, Partners for Prosperity, LLC

Life insurance types

If you are searching for affordable life insurance, a term policy may prove to be the best choice. Term life insurance offers financial protection over a set period of time. Term policies can range from as short as one year to thirty years or longer. The length of your term is your choice but is often related to your need, according to this California Department of Insurance guide. For instance, you may want a term policy that will last as long as you are making payments on your mortgage or as long as your children are under 18.

On the other hand, cash value life insurance provides more financial flexibility in comparison to term life insurance. Cash value life insurance is a permanent form of life insurance that accumulates value over the course of a policyholder’s lifetime. Additionally, a cash value policy may offer tax benefits unavailable with term coverage.

Most companies offer Universal and Whole Life insurance policies. If you buy a Universal Life Insurance plan, you’ll pay at least a minimum premium with the option of paying in more as an investment. The downside is, you can’t choose your own investment options. Most of the time your funds are invested in mutual funds or bonds.

A Whole Life Insurance policy is a permanent policy that covers you through the length of your life and pays a predetermined amount to your beneficiary when you die. One major benefit of a Whole Life Insurance policy is your premieum will never increase during your lifetime.

Life insurance amount

There is no golden rule to help you decide exactly how much life insurance coverage or which type of policy to buy. Instead, you’ll need to evaluate your age, income, lifestyle and other factors to obtain the right coverage. If you need some frame of reference for your insurance needs, consider the following policy value frameworks.

A 5-10 times income rule of thumb approach often helps people purchase the right amount of coverage, according to the Wall Street Journal’s Jeff D. Opdyke. As the rule implies, the 5-10 times income approach will require you to look at your current income and multiply it by 5 to 10. Then, you can purchase life insurance coverage for this total to ensure optimal financial protection for your loved ones.

Estimate your coverage amount

Alternatively, the DIME formula helps determine life insurance coverage needs as well. This formula involves looking at your Debt, Income, Mortgage and Education expenses (D-I-M-E). Next, you’ll need to add these figures together to determine your ideal life insurance coverage amount.

Life insurance costs

When it comes to life insurance, it helps to shop around. Some life insurance companies may claim to offer the best coverage at the best price, but you won’t know whether this is true unless you explore all of your options. Costs will vary depending on your age, your lifestyle, and other factors.

The main unit for determining life insurance rates is the cost per $1,000 of insurance. For example, if the rate is $0.3 per $1,000 and an enrollee selects $15,000 of coverage, the monthly premium will be $4.50 ($0.3 x 15 = $4.50).

Moreover, employers often subsidize the cost of a policy, so you’ll find getting coverage on your own may be priced differently than you expect. For instance, according to a biweekly cost table for New York state employees, the biweekly cost per $1,000 of coverage is for a 50-54 year old non-smoker is $.08. The IRS provides a reference price for group term insurance prices:

| Policy Holder’s Age | Monthly Cost Per $1,000 of Protection |

|---|---|

| Under 25 | $0.05 |

| 25-29 | $0.06 |

| 30-34 | $0.08 |

| 35-39 | $0.09 |

| 40-44 | $0.10 |

| 45-49 | $0.15 |

| 50-54 | $0.23 |

| 55-59 | $0.43 |

| 60-64 | $0.66 |

| 65-69 | $1.27 |

| 70 and older | $2.06 |

Once you find the right life insurance company, add your premium payments to your monthly budget. It may be beneficial to set up automatic withdrawals from a bank account or credit card to ensure seamless coverage. Or, you can make monthly payments on your own to avoid a lapse in coverage.

Life insurance agent vs broker

Insurance agents and brokers can teach you about a broad array of life insurance options. An insurance agent works exclusively for one insurance company, whereas an insurance broker sells insurance from a variety of insurers. As such, insurance agents and brokers may play key roles in your ability to secure the best life insurance coverage at the lowest price.

Regardless of whether you work with an insurance agent or broker, it is typically a good idea to reach out to insurance professionals for support. If you meet face to face with an insurance agent or broker, you can receive real-time responses to your life insurance questions.

Reassess your life insurance policy every 5 years

Life can change at a moment’s notice. And as you grow older, it helps to reexamine your life priorities, as well as your life insurance policy. This will enable you to financially protect your loved ones, no matter what happens.

In many cases, life insurance costs will increase as you age. This means you may need to allocate additional funds to cover your life insurance expenses. Of course, many life insurance companies offer health incentives to policyholders. If you quit smoking, lose weight or drive safely, you may be able to reduce your life insurance premiums.

Our Search for the Best Life Insurance Companies

- We searched for an extensive list of life insurance companies

- We evaluated life insurance companies based on our expert-guided buying criteria: customer support, affordability, and coverage options

- We provided you the best life insurance companies for consideration

Searching for the right life insurance company may be a difficult process. Luckily, we did the hard work for you. Our in-depth life insurance company analysis focuses on each insurer’s industry reputation, policy offerings and other criteria.

Our search began with 17 of the largest life insurance companies. It included the following steps:

- We started with a comprehensive list of life insurance companies. We developed a list of 17 of the most widely recognized companies, since these were the most likely to be selected by consumers. If the company didn’t sell nationally, it was cut from our preliminary list.

- We looked for industry ratings and awards. We wanted to find the top life insurance companies in terms of customer support, affordability and coverage options. We examined life insurance company ratings from A.M. Best, J.D. Power, and other prominent independent research firms, looking for accolades related to customer support, affordability and coverage. Companies that weren’t mentioned in the news were cut from our list.

- We shopped for life insurance and followed our own advice. We focused on finding life insurance companies based on our wise buyer criteria. We evaluated the different types of life insurance policies provided by each company, the costs associated with each coverage option and what consumers had to say.

If a life insurance company failed to define life insurance terms to its clientele, was rated below 4 stars on popular review sites, or was difficult to shop, we excluded it from our search.

Life Insurance Company Reviews

AAA Life Insurance Review

Great Customizable Coverage

Screenshot: AAA Life Insurance

AAA Life Insurance Company has been providing for families, individuals and seniors since 1969. The company offers two term, whole life and universal life insurance policies with several riders to customize coverage. Most AAA Life Insurance policies and annuities do not require a AAA membership, but members receive discounts on premiums.

AAA Life Insurance offers term policies to individuals up to age 85. You can apply for an ExpressTerm policy online and know in 10 minutes if you’re approved. Whole life insurance is available for people up to age 85. AAA Life Insurance whole life policies have four optional riders, and the Guaranteed Issue Whole Life requires no medical exam. Choose from several riders with a universal life policy, and Accumulator Universal Life lets you set your premium amounts.

Three annuities round out AAA Life Insurance Company’s products. Two deferred annuities require a minimum investment of $3,000. The Guaranteed Income Annuity has a higher minimum but has perks like the Increasing Benefit option to keep your income stream at pace with inflation.

AAA members can buy accident insurance to pay for emergency room and medical bills. This policy also has a death benefit. Membership is not a requirement for other policies.

Learn more about policies offered by AAA Life Insurance Company, by visiting their website.

Leap Life Review

Great Policy Matching

Screenshot: Leap Life

Leap Life is a life insurance broker who partners with highly-rated companies like Protective Life, American General, Mutual of Omaha, Pacific Life, Transamerica and more. Its partner brands are all highly-rated for financial strength with AM Best. Essentially a one-stop shop for life insurance quotes, Leap Life gives you the ability to shop life insurance policies from one website while chatting with insurance experts to find a policy that fits your needs.

Leap Life uses Artificial Intelligence (AI) technology to find the right life insurance policy for your personal circumstances. Leap Life’s AI technology takes the information you provide (health history, age, location and financial situation) and checks it against their partner life insurance companies’ underwriting guidelines, giving you a quote with the best deal from multiple life insurance companies. Leap Life highlights include:

– Savings of up to 40-300% with Leap Life matching technology

– $100,000 and $5,000,000 in coverage limits

– 10, 15, 20, and 30 year terms available

– No extra fees and free 30-day returns

Leap Life holds an “A+” rating with the Better Business Bureau. Read our full Leap Life review for more details.

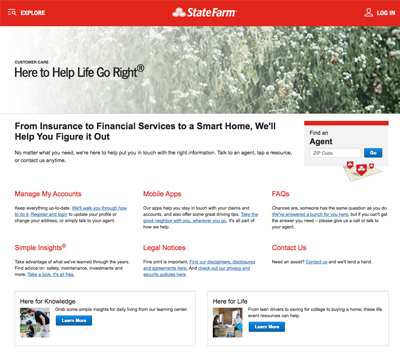

State Farm Review

Great Service

Since 1922, State Farm has provided insurance to help life go right. State Farm boasts more than 65,000 employees and 18,000 independent contractor agents. The life insurance company also provides a convenient website, making it easy for you to get in touch with local life insurance agents any time you choose.

Screenshot: State Farm

If you’re unfamiliar with life insurance and searching for an instant quote, there may be no better choice than a visit to State Farm’s website. Here, you can quickly get a life insurance quote, regardless of where you live. State Farm even offers “Coverages at a Glance,” which outlines the similarities and differences between assorted life insurance policies. This enables you to learn about different types of life insurance and make an informed selection before you retrieve a life insurance quote.

State Farm ranked first in terms of overall satisfaction in the 2016 J.D. Power Life Insurance Study. Many customers enjoy State Farm’s website, and customers frequently say the site simplifies the process of finding nearby agents and managing claims. State Farm offers a Pocket Agent mobile app too, and this app enables policyholders to view policy information, get quotes and submit and manage claims from their smartphones and tablets.

To learn more about State Farm Life Insurance Policies, read our comprehensive State Farm review.

Haven Life Review

Most Affordable

For those who want to simplify life insurance, there’s Haven Life. This life insurance company is backed by MassMutual and provides term coverage for individuals up to 65 years old.

Screenshot: Haven Life Insurance

What separates Haven Life from other life insurance companies is its InstantTerm application and approvals process, which only requires about 20 minutes to complete. InstantTerm enables individuals up to the age of 45 years old to finalize coverage without a medical exam. It also is supported by state-of-the-art approvals technology, enabling life insurance applicants to receive a coverage decision in just minutes. Meanwhile, the average monthly cost of a Haven Life term policy is $21, which means you likely won’t have to break your budget to purchase high-quality coverage from this life insurance company.

Haven Life policyholders frequently rave about the company’s speed and efficiency, particularly when it comes to its application and approvals process and customer service. Additionally, Haven Life boasts a 9.3 out of 10 average rating from more than 200 client reviews on TrustPilot and a 4.5 out of 5 stars rating on ConsumerAffairs.

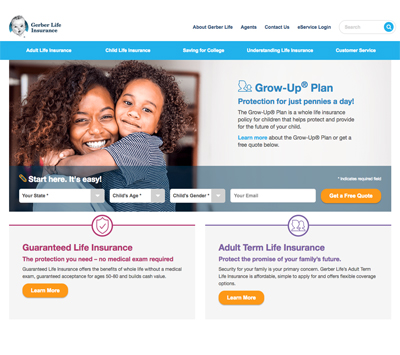

Gerber Life Insurance Review

Great Coverage Options

Gerber Life Insurance is an affiliate of the Gerber Products Company, also known as “the baby food people.” It has a simple goal: to empower parents with the ability to provide financial security to their respective families. To accomplish this goal, Gerber Life Insurance offers a vast selection of coverage options.

Screenshot: Gerber Life Insurance

Many Gerber Life Insurance plans are available, but perhaps none are more popular than the company’s Grow-Up® Plan. This cash value life insurance policy is designed to help kids accumulate up to $50,000 of life insurance coverage. It can be purchased for kids between the ages of 14 days and 14 years old and offers affordable premiums. Additionally, Gerber Life Insurance provides term and cash value adult life insurance policies. It also offers online resources such as an FAQ and “Life Insurance Terminology” list to teach adults the ins and outs of life insurance.

Currently, Gerber Life Insurance provides more than $45 billion in coverage across 3.3 million life insurance policies. Gerber Life Insurance received an “A” (Excellent) rating from A.M. Best in May 2017, and many customer reviews highlight the company’s value for money and ease of doing business.

To learn more about Gerber’s Life Insurance Policies, read our comprehensive Gerber Life Insruance review.

Additional Life Insurance Companies

– Prudential Life Insurance offers four life insurance policies: Term, Universal, Indexed Universal and Variable Universal. Read our comprehensive Prudential Life Insurance review.

Related Life Insurance Resources

Readers of this life insurance guide also found these related articles helpful.

Life Settlements: How to Sell Your Life Insurance Policy

If you find yourself needing to sell your life insurance policy but don’t know where to start, read about the life settlement process, how much money you can expect to receive from a life settlement and alternatives to life settlements.

Frequently Asked Questions

What is life insurance?

Life insurance represents a contract between an individual and an insurer. Under a life insurance policy, the insurer will pay a lump sum, aka “death benefit,” upon a policyholder’s death. This lump sum will be paid to the person you name as your life insurance beneficiary stipulated by a policyholder, and beneficiaries may use the funds toward mortgages, student loans and various everyday expenses.

Can I purchase life insurance for someone else?

Anyone can purchase life insurance, at any time. However, you can buy life insurance for someone else only if you can verify this person’s death would negatively affect your finances. Also, you will need a person’s consent to buy life insurance for him or her. A life insurance company will likely require this individual to complete a medical exam as well.

How much life insurance do I need?

The amount of life insurance a person needs varies based on his or her income, living expenses and other factors. To determine the ideal amount of life insurance coverage, an individual should evaluate how much money will be required to help his or her loved ones meet their everyday financial obligations. We came across this human life calculator during our research to help you assess the financial loss your family would take on if you were to pass away.

Will I have to get a medical exam to obtain life insurance?

In all likelihood, yes. A medical exam is a standard requirement of the underwriting process for most traditional life insurance policies. Some no-medical-exam life insurance plans are available. However, these plans commonly feature lower coverage amounts and higher premiums than life insurance policies subject to the full underwriting process.

How does life insurance payout?

A life insurance policy pays out after a policyholder dies. At this time, a beneficiary or beneficiaries will file a death claim with the life insurance provider. Next, the life insurance company will process the claim; most states provide the insurer with 30 days to review the claim and accept, deny or ask additional questions about it. If the insurance company approves the claim, the beneficiary or beneficiaries usually will receive a lump sum payout within 30 to 60 days of the initial claim date.

Concluding Thoughts on Life Insurance

Bottom Line:

Life insurance provides financial protection to your loved ones after you pass away.

There are lots of life insurance companies, but choosing the insurer with the lowest premium or highest coverage amount offers no guarantees. Ideally, the right life insurance company offers a combination of affordability and superb coverage and is backed by exceptional customer support.

The three life insurance companies we recommended stand out for different reasons but meet our criteria for the best life insurance companies. We drew these conclusions after performing extensive market research and expert analysis. Our recommendations are designed to help you streamline your life insurance search and find the right plan based on your specific needs. Hopefully, our recommendations can help you make the best possible life insurance decision.

| Expert Review | Company | |

|---|---|---|

| 1 | Great Budget Options | TruStage Life Insurance |

| 2 | Great Comparison Shopping | SelectQuote |

| 3 | Great Online Marketplace | Reliaquote |

| 4 | Great Term Insurance | Fidelity Life Insurance |

| 5 | Life Insurance Calculator | Everyday Life Insurance |

| 6 | Great For Healthy Individuals | Health IQ |

| 7 | Great Policy Matching | Leap Life |

| 8 | Great Reliability | AIG Direct |

| 9 | Great Customizable Coverage | AAA Life Insurance Company |

| 10 | Great One-Stop Shopping | Policygenius |

| 11 | Great Service | State Farm |

| 12 | Great Value | Gerber Life Insurance |